The Spiritual Growth of Wealth Redistribution

![]() Over 10 years ago I went to live, study and work in the Santi Asoke community in Thailand. The Asoke group are fundamentalist Thai Buddhists who are building an anti-capitalist economy based on the economic model of bunniyom. Bunniyom is the pursuit of merit, whereas thunniyom, the Thai word for capitalism, is about the pursuit of profit. The Asoke community believes that merit and profit are in opposition. When you make a profit, you lose karma. Their economy is centered on practices that generate positive karma, such as selling goods at cost, and festivals where goods are offered for free. I loved how the Asoke communities’ spiritual beliefs had drastically shifted the way they participated in the economy. I wanted to contribute towards building an economy framed around wealth redistribution and spiritual growth in the United States.

Over 10 years ago I went to live, study and work in the Santi Asoke community in Thailand. The Asoke group are fundamentalist Thai Buddhists who are building an anti-capitalist economy based on the economic model of bunniyom. Bunniyom is the pursuit of merit, whereas thunniyom, the Thai word for capitalism, is about the pursuit of profit. The Asoke community believes that merit and profit are in opposition. When you make a profit, you lose karma. Their economy is centered on practices that generate positive karma, such as selling goods at cost, and festivals where goods are offered for free. I loved how the Asoke communities’ spiritual beliefs had drastically shifted the way they participated in the economy. I wanted to contribute towards building an economy framed around wealth redistribution and spiritual growth in the United States.

After studying Buddhist economics, and working at Schumacher Center to learn more about local economics, I got involved in the Occupy Wall Street movement. I was fired up, and I was also a member of the 1%. I began to feel urgency around understanding my family’s wealth, my own wealth, and shifting my investments into alignment with my values. I wanted to move money off of Wall Street onto Main Street, and I was learning how to do that through my work doing research for local investing visionary Michael Shuman.

Local investing was an important shift for me. I began to build strong, transparent relationships with entrepreneurs. I saw how the structure of the loan shaped the financial reality of the borrower, and had the power to shift the economic reality of marginalized communities and entrepreneurs. I also noticed that when I went to local investing conferences and meetings, I saw mostly white, wealthy investors lending money to white, class-privileged entrepreneurs. I was reaching some entrepreneurs of color in my networks, but it seemed like my lending wasn’t redistributing wealth or power.

Around that time, I attended my first Resource Generation conference. Resource Generation is a powerful organization bringing together young people with wealth to work towards the equitable distribution of land, wealth, and power. I began to understand that my decisions about how to move the money I inherited could be a part of a broader movement, a movement that could build power for marginalized communities, fund grassroots organizing, and resource the emerging solidarity economy.

What Does an Investment Portfolio that Centers on Wealth Redistribution Actually Look Like?

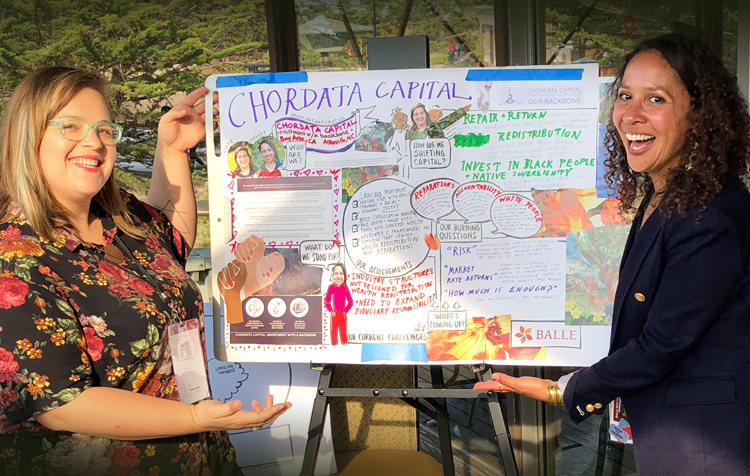

There are so many ways we talk about aligning our investments with our values. I often talk about being in the impact investing space because I believe in the power of moving investments out of public equities and into direct investments. I also am a practitioner of Integrated Capital, an approach developed by Leslie Christian, Joel Solomon, and RSF Social Finance, that includes using diverse forms of capital (including giving and investing) to address injustices and imbalances in our economy. After ten years of researching and experimenting with values-aligned investing, I realized I could do my most powerful work as an investment advisor. Tiffany Brown and I co-founded Chordata Capital, and joined the Natural Investments team. Together we’ve developed a backbone to our investing and advising work that includes an explicit commitment to racial and economic justice, accountability and shared risk-taking, and bringing an embodied, spacious approach.

Tiffany and I build investment portfolios that center on racial and economic justice. We know poor people are the real experts on poverty, black activists are experts on anti-black racism, and any attempt to solve a social problem must be shaped and guided by those affected. Racial and economic justice requires wealth redistribution, including a commitment to both building wealth in black, brown, poor, and immigrant communities and a commitment to ending wealth accumulation and hoarding in white, wealthy communities. Closing the racial wealth divide isn’t simply about lending money to people of color (POC) entrepreneurs. It includes white wealthy people choosing to give more money away and invest it in ways that decrease their total wealth over time. Closing the racial wealth divide requires wealthy people to support the infrastructure that grassroots movements for racial and economic justice were building to set up and run community-controlled loan funds. [1]

Advice for Millennials about Money

Thinking about and talking about money has a huge impact on how we understand ourselves, our families and our relationships. My advice to millennials about money is to find spiritual and embodiment practices that support you as you navigate financial conversations and decisions. Those personal practices can serve as a foundation for working in community to do transformational money work. My practices are rooted in community and relationship.

Like many generations before us, we live in a complicated, frightening and expansive political moment. Unlike generations before us, much of the technology and culture we are immersed in has been built to fragment and isolate us. We need each other. Our work is more powerful and grounded when it is anchored in loving, accountable relationships. You don’t have to do this work alone, and you shouldn’t do this work in isolation. If you’re in the top 10%, connect with your local chapter of Resource Generation. If you’re not wealthy but looking for radical financial resources check out – Ride Free Fearless Money. And start those difficult but fascinating conversations with your friends and family about wealth, money, giving and investing.

For me, the work of redistributing wealth and power required both communities of practice (like Resource Generation) and personal practices. My personal practices include meditation, journaling, therapy, dance, and making art. These practices support my capacity for experimentation and vulnerability, core competencies for making bold moves with my money.

There’s a need for healing and repair in our economy. Massive redistribution of wealth is required to address the history of violence, extraction, colonization, slavery and oppression that are the foundation on which wealth has been built in this country.[2] We need reckoning and reconciliation on a national scale, on a personal scale and in our investment portfolios.

Article by Kate Poole, an investment advisor at Natural Investments and co-founder of Chordata Capital. Kate works with people who have inherited wealth to design and implement investment portfolios that embody an explicit commitment to racial and economic justice.

She started her work in the new economy field at Schumacher Center for New Economics after graduating from Princeton University in 2009, where she wrote her thesis on the intersection of spiritual beliefs and economic action. She went on to work with Michael Shuman, researching local investing for his books Local Dollars, Local Sense and The Local Economy Solution. She co-founded Regenerative Finance in 2014 to organize other young people with wealth to shift control of capital to communities most affected by racial, economic and environmental injustices. In 2017 she was an RSF Integrated Capital Fellow.

She is a member of Resource Generation, organizing young people with wealth to redistribute land, wealth and power, and she serves on the board of directors of the Schumacher Center for New Economics and the New Economy Coalition.

Kate Poole and Tiffany Ann Brown, the principals of Chordata Capital, are investment advisory representatives of Natural Investments LLC. Natural Investments is an independent Registered Investment Advisor firm. Chordata Capital is not a registered entity and is not an affiliate or subsidiary of Natural Investments.

Article NOTES:

[1] The infrastructure I support includes:

• Working World’s Financial Cooperative – https://www.theworkingworld.org/us/peer-network

• The New Economy Coalition – https://neweconomy.net

• The Runway Project – https://www.therunwayproject.org/oakland

• The Ujima Fund – https://www.ujimaboston.com

• The Buen Vivir Fund – https://thousandcurrents.org/buen-vivir-fund

[2] To learn about the racist history of wealth accumulation in this country you can read:

• Decolonizing Wealth by Edgar Villanueva – http://decolonizingwealth.com

• Restorative Economics by Nwamaka Agbo – https://www.nwamakaagbo.com/restorative-economics

or connect with or attend trainings by:

• United for a Fair Economy – http://www.faireconomy.org

• Resource Generation – https://resourcegeneration.org

While difficult at the moment, the conversations with my friends about money inspired me to explore a different path. Conversation after conversation, I started to chip away at what felt wrong about money, and we would talk about their “wish list” when it comes to finance. What came up again and again was the desire to feel smart about money decisions – “whatever I do should be easy to understand, available to all, convenient to do, and make me feel good and empowered.”

While difficult at the moment, the conversations with my friends about money inspired me to explore a different path. Conversation after conversation, I started to chip away at what felt wrong about money, and we would talk about their “wish list” when it comes to finance. What came up again and again was the desire to feel smart about money decisions – “whatever I do should be easy to understand, available to all, convenient to do, and make me feel good and empowered.” We tend to underestimate the collective power our money can have. Even just a few hundred dollars from a few hundred people can drive significant change. That’s why I named my company CNote; it’s slang for “$100 bill” and short for “Community Note.” Together, our $100s become $millions, and these millions have tremendous power. To illustrate, CNote members have already helped create and maintain over 2,000 jobs in America, and that’s just the beginning.

We tend to underestimate the collective power our money can have. Even just a few hundred dollars from a few hundred people can drive significant change. That’s why I named my company CNote; it’s slang for “$100 bill” and short for “Community Note.” Together, our $100s become $millions, and these millions have tremendous power. To illustrate, CNote members have already helped create and maintain over 2,000 jobs in America, and that’s just the beginning.