10 Years of Green Bonds: From Evolution to Revolution

Issued in November 2008, the World Bank’s first green bond created the blueprint for sustainable investing in the capital markets. Today, the green bond model is being applied to bonds that are raising financing for all 17 Sustainable Development Goals.

The phone call to the World Bank Treasury came out of the blue: a group of Swedish pension funds wanted to invest in projects that help the climate, but they did not know how to find these projects. But they knew where to turn and called on the World Bank to help. Less than a year later, the World Bank issued the first green bond—and with it, created a new way to connect financing from investors to climate projects.

Bonds are essentially an agreement where issuers borrow funds from investors and must repay investors at an agreed rate after a specified amount of time. Governments, companies and many others issue bonds to borrow money for projects. Issuing a bond was nothing new for the World Bank—it is how the institution finances its lending for development projects since 1947. But the concept of a bond that is dedicated to a certain kind of project had not been tested before. It turned out to be a history-making event that fundamentally changed the way investors, development experts, policymakers, and scientists worked together.

A Stark Warning

In 2007, the Intergovernmental Panel for Climate Change—a United Nations agency that provides scientific data on climate change and its political and economic impacts—published a report that undeniably linked human action to global warming. The finding, along with increasing occurrences of natural disasters, prompted a group of Swedish pension funds to think about how they could use the savings they were stewarding toward a solution. They called on their bank, SEB (Sandinaviska Enskilda Banken AB) to see what could be done. And SEB connected the dots between the financing that was seeking to reduce risks for the investors and make a positive impact, and the World Bank with its deep knowledge on investing in environment projects around the world.

Thinking Outside the Box

In hindsight, the solution seems straightforward. Investors wanted a safe place to put their money and know that they were making a difference. The World Bank had environment projects to finance, a track record as a high-quality bond issuer, and the ability to report on the impact of its projects. But there was a missing link: how could investors be truly certain that the projects they were supporting addressed climate concerns?

This triggered another phone call, this time to CICERO, the Centre for International Climate and Environmental Research — an interdisciplinary research center for climate research in Oslo. CICERO scientists were leading experts on climate issues. They could provide a credible view on whether a project was going to make a positive impact on the environment.

What followed were many more conversations among the pension funds, SEB, CICERO, and the World Bank Treasury. The conversations were often difficult—especially since more often than not, the different organizations spoke different languages, and it was challenging to bridge the gap between finance, development and science.

“Green bonds help investors address the environmental, social or governance risks that can have a material effect on returns.” – Heike Reichelt, Head of Investor Relations and New Products, The World Bank Treasury

A Joint Commitment to Finding a Solution

Success ultimately came in November 2008, when the World Bank issued the green bond. The bond created the blueprint for today’s green bond market. It defined the criteria for projects eligible for green bond support, included CICERO as a second opinion provider, and added impact reporting as an integral part of the process. It also piloted a new model of collaboration among investors, banks, development agencies and scientists. Ultimately, it was the result of their commitment, perseverance, and drive to find a solution.

The World Bank green bond raised awareness for the challenges of climate change and demonstrated the potential for investors to support climate solutions through safe investments without giving up financial returns. It formed the basis for the Green Bond Principles[1] coordinated by ICMA, the International Capital Markets Association. It highlighted the social value that bonds could create and the need for a sharper focus on transparency.

Since then, the World Bank has raised US$13 billion through more than 150 green bonds in 20 currencies for institutional and retail investors all over the globe. Other green bond issuers now include companies and banks of all sizes and several countries. All issuers are measuring, tracking and reporting on the social and environmental impact of their investments. Fannie Mae is the largest issuer of green bonds by volume in a single year. Fiji last year issued the first emerging market sovereign green bond. Every bank active in the international capital markets has staff dedicated to green or sustainable bond financing. Green lending criteria are being incorporated in loans. There is an industry of second opinion providers and verifiers, including rating firms and others providing information to investors and supporting issuers.

A Sustainability Revolution

Fast forward ten years. Capital markets have evolved from a market where investors knew and cared little about what their investments were supporting, to one where purpose matters more than ever. The basic green bond premise—with its model for project selection, second party opinion, and impact reporting—is being applied to other areas. As a result, there are now social bonds, blue bonds, and other bonds that raise financing dedicated to a specific development purpose. All follow the green bond model with its focus on impact reporting. More than US$500 billion in these kinds of labeled bonds have been issued since 2008.

![]()

Investors’ interest in the social and environmental purpose of their investments reflects a fundamental shift in the bond market. Investors understand their power to support initiatives their stakeholders care about, that they do not have to give up returns. They also want data that shows how they are addressing environmental, social and governance factors — particularly as they and they increasingly understand that in addition to creating social value, they are mitigating risk to their own investments. An issuer with good sustainability practices will generally be a better investment. Issuers are responding. Issuers are engaging with investors to show how their bonds present opportunities to achieve both financial and social returns.

Investors are looking beyond the narrow market of labeled bonds to understand how issuers use their investments. That market is much larger – the World Bank alone issues US$50 billion every year in Sustainable Development Bonds for its development lending.[2]

This revolution was sparked by green bonds. The challenge now is to build on the momentum. The Sustainable Development Goals (SDGs) are a collection of 17 global goals agreed by 193 countries in 2015 that range from education to health and sustainable cities. The SDGs are a helpful framework for investors and issuers to focus on areas beyond climate. The World Bank has started to engage investors around specific SDGs through a series of bonds to raise awareness for specific development challenges through its sustainable development bonds. Others are following.

For more information and to read the The World Bank Green Bond Impact Report 2018 visit – http://treasury.worldbank.org/en/about/unit/treasury/ibrd/ibrd-green-bonds

Article Notes

[1] https://www.icmagroup.org/green-social-and-sustainability-bonds/green-bond-principles-gbp

[2] http://treasury.worldbank.org/en/about/unit/treasury/ibrd/ibrd-sustainable-development-bonds

Additional Articles, Energy & Climate, Impact Investing, Sustainable Business

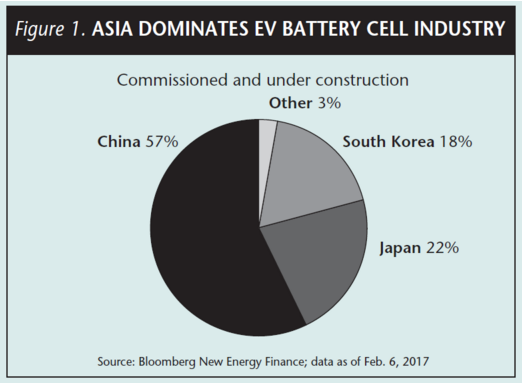

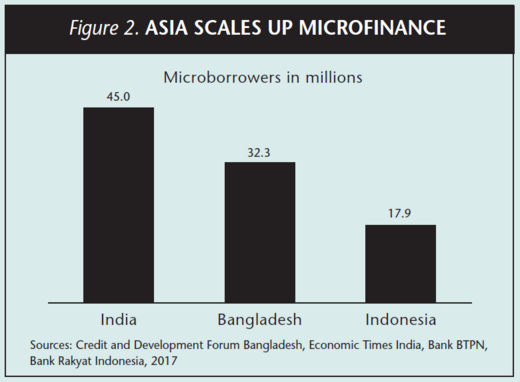

For investors interested in environmental, social and governance (ESG) strategies, a regionally diversified approach can help capture global growth. In the coming year, Asia offers a prime opportunity to invest in profitable companies addressing critical ESG challenges through robust and sustainable business models. ESG innovation in Asia is evident across many sectors, including health care and pharmaceuticals, technology, finance and alternative energy. To fully capture the growth and profits of the world’s most innovative ESG companies, it is worth considering Asia. Here, we identify three ESG trends in Asia to watch in 2019.

For investors interested in environmental, social and governance (ESG) strategies, a regionally diversified approach can help capture global growth. In the coming year, Asia offers a prime opportunity to invest in profitable companies addressing critical ESG challenges through robust and sustainable business models. ESG innovation in Asia is evident across many sectors, including health care and pharmaceuticals, technology, finance and alternative energy. To fully capture the growth and profits of the world’s most innovative ESG companies, it is worth considering Asia. Here, we identify three ESG trends in Asia to watch in 2019.