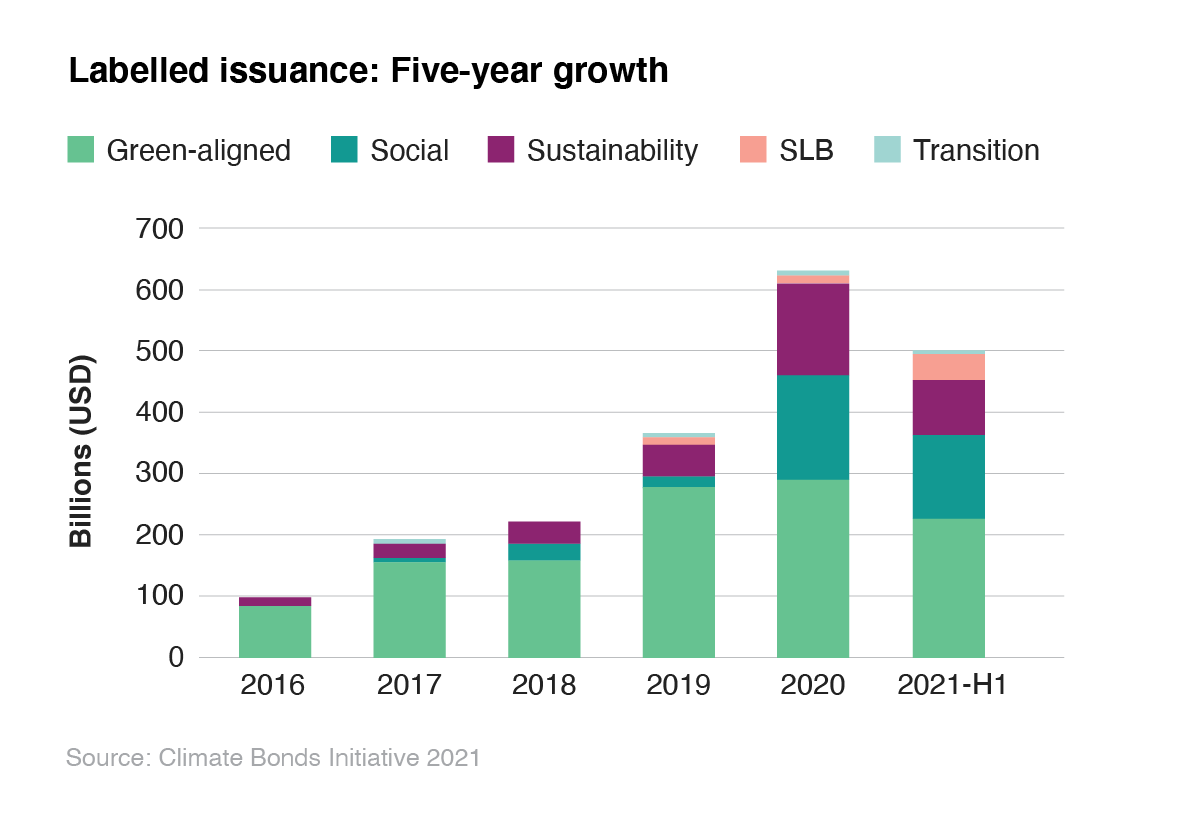

The green bond market, which is anticipated by Climate Bonds Initiative (CBI) to reach $1 trillion annually by 2023, has played an increasingly important role in financing assets needed for the transition to a low-carbon future. In 2021 labelled green bond issuance as a percentage of the total has grown to 20% in Europe and 3% in the US, with green bonds making up approximately half of all labelled bonds ($356.2 billion in YTD issuance) and instruments with other green elements (sustainability and sustainability-linked bonds) comprising more than half of the remainder.1 Issuers from 47 different countries executed a green debt deal in the first half of 2021 alone.2

The green bond market, which is anticipated by Climate Bonds Initiative (CBI) to reach $1 trillion annually by 2023, has played an increasingly important role in financing assets needed for the transition to a low-carbon future. In 2021 labelled green bond issuance as a percentage of the total has grown to 20% in Europe and 3% in the US, with green bonds making up approximately half of all labelled bonds ($356.2 billion in YTD issuance) and instruments with other green elements (sustainability and sustainability-linked bonds) comprising more than half of the remainder.1 Issuers from 47 different countries executed a green debt deal in the first half of 2021 alone.2

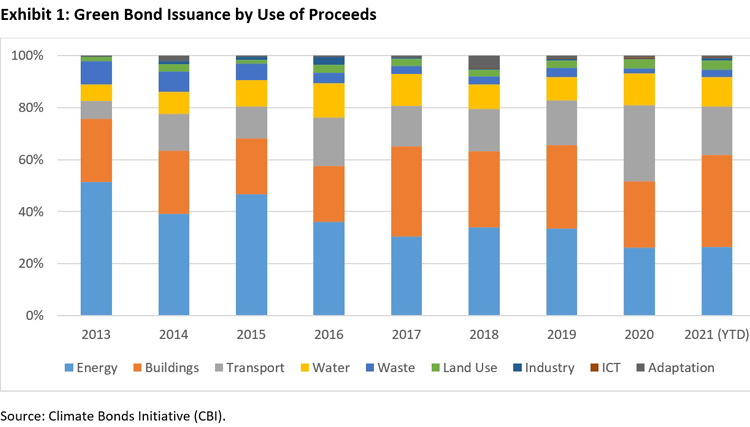

The collective focus on green project categories that address climate change mitigation-related issues (such as energy, buildings and transport) has remained strong despite the expansion of the market — likely due to increasing adoption of climate targets at national and organizational levels (Exhibit 1).

This growth, however, has outpaced the development of precise global standards and guidance as to which bonds qualify as “green.” This creates present-day hurdles for issuers and investors, placing further market growth at risk to the extent that trust in the “green bond” label could falter in the context of growing scrutiny over investment funds’ possible greenwashing. Many standard-setting bodies have recently sought to address this issue.

Standardization Aims to Increase Confidence, Credibility

While use of bonds proceeds fairly quickly coalesced around the guidelines laid out in the International Capital Market Association’s (ICMA’s) Green Bond Principles,3 certain corners of green finance continue to grapple with uncertainty. Some issuers remain doubtful as to whether their projects have sufficient impact to qualify in the green financing market. Others fear their perception among ESG investors as a non-green entity may disqualify them from participation.

Some notable guidance has emerged since the beginning of 2020. One key area is “transition” finance, where companies in higher-carbon-emitting industries and businesses look to pursue a greener path. In September 2020, CBI and Credit Suisse published “Financing Credible Transitions,” a framework that defined specific principles for an ambitious climate transition strategy and proposed a set of labels for economic activities along the spectrum from net-zero aligned to stranded to bring clarity to potential entrants to the transition bond market. In December 2020, ICMA released its “Climate Transition Finance Handbook”, which delivered issuer-level recommendations on the disclosure necessary to generate trust from investors regarding transitions, even if it did not provide a definitive framework for defining transition bonds as some had hoped. Broader frameworks like the Transition Pathway Initiative and IEA Net Zero by 2050 Roadmap help to define the credibility of issuer transition strategies and trajectories to date. CBI contributed further to this effort in September 2021 with the publication of a discussion paper on transition finance for transforming companies. This document proposed “hallmarks of a credibly transitioning company” — adoption of Paris-aligned targets, and evidence of robust plans and governance, implementation action, internal monitoring, and transparent reporting — to encourage the disclosure of material and decision-useful information by issuers, and to assist investors in their evaluation of the adequacy of an issuer’s transition.

Investor concerns generally center on whether they have adequate information to make well-informed decisions. Greater formalization of transition benchmarking and green bond qualifications is expected to provide “confidence for investors, credibility for issuers and clarity for bankers.4 This, in turn, could promote greater market growth in high-emitting areas of the economy.

EU Taxonomy Advances

The European Union (EU) has established a sustainable activities taxonomy set to underpin the EU Green Bond Standard and serve as a benchmark for a bond’s alignment with six key environmental objectives. The first delegated act on sustainable activities for two of those objectives — climate change mitigation and climate adaptation — was adopted in June 2021, with preliminary recommendations for the remaining four objectives (water, circular economy, pollution prevention & control, and biodiversity & ecosystems) also published earlier this year. The EU taxonomy will provide significant guidance to investors and issuers worldwide on what economic activities may be considered sustainable and the metrics that can be used to make such determinations and may serve as an effective template for other regulatory regimes that seek to provide similar guidance to markets.

China Raises its Standards

China has historically been the only major center of green bond issuance where a significant percentage of green bonds consistently fall short of broadly accepted international standards. However, it has recently made significant headway in raising its green bond qualification standards.

In May 2020, the People’s Bank of China (PBOC), China’s central bank, released a consultation draft of its 2020 Green Bond Catalogue, which removed “clean utilization of fossil fuel” projects from its list of programs eligible to be funded by green bonds. The final draft was published in April 2021, along with a commitment from PBOC Governor Yi Gang to introduce more consistent rules on disclosure. These updates also consolidated standards for issuers across China’s disparate jurisdictions that were previously overseen by several different regulators. The National Development and Reform Commission (China’s state economic planning ministry) and China Securities Regulatory Commission jointly rolled out the new Green Bond Catalogue with the PBOC. This provided a more coherent view on acceptable green projects in the country. Differences remain between these sometimes less-stringent standards and internationally accepted green project categories, such as their allowance for natural gas-fired power generation, indicating some level of dislocation is still likely to persist.

Reporting Needs

Reporting on labeled green bond issuance is one of the more fragmented elements of the market, and it remains a challenge for advisors to reflect the impact of their investments to clients. While most issuers of labeled debt today explicitly commit to reporting on the impact of their securities, this has not always been the case. Moreover, such reporting arrives to investors in a variety of formats with varying levels of granularity, timeliness and disclosures of underlying assumptions.

Third-party efforts such as the ICMA Harmonized Handbook for Impact Reporting and the NPSI Position Paper on Green Bonds Impact Reporting have emerged as best-practices frameworks to enable effective impact reporting.

Investors can accelerate impact metrics development by telling issuers what information they deem most critical and what they regard as market best practices. As engagement with issuers, consultants and banks continues, we expect to see greater market growth and comprehensive green bond standards formalized.

Potential Pitfalls

Although regulatory guidance on the definition of environmentally sustainable investments has been broadly anticipated by the market and is seen as a necessary step, the rapid growth of initiatives risks additional complexity as well. The Future of Sustainable Data Alliance recently published an overview of the various taxonomy projects underway around the world, detailing five regulations already in place, three in draft, 15 under development and two being discussed as a possibility. With notable exceptions, such as the regionally applicable regulations developed by the EU and the ASEAN Taxonomy Board, these regulations are commonly established at the country level, indicating more may yet arise.

As different bodies strive to provide the market with the standardization it is looking for, they risk solidifying differing regional or national definitions of “green” and creating a complex web for issuers, investors and other stakeholders to navigate. Nevertheless, the institution of taxonomies around the globe, so long as they operate on fundamentally similar principles, may provide a much greater benefit in terms of reducing greenwashing concerns. Efforts are already underway to institute “Common Ground” taxonomies, such as the one in development between the EU and China as part of the International Platform on Sustainable Finance (IPSF).

The green bond market is critical to financing the global transition to a more environmentally sustainable society in line with scientific targets. Calvert’s process for evaluating green bonds places a focus on the trajectory and intentionality of issuers in addition to the qualities of financed assets to parse the true impact of green bonds, but even for sophisticated green bond investors, improved disclosure and standardization of green and sustainable bond classifications will help facilitate meaningful investment analysis in addition to promoting broader market growth.

Article by Henry Mason, an ESG senior research associate for Calvert Research and Management; and Brian Ellis, a vice president and portfolio manager for Calvert Research and Management

See their biographies below.

The value of investments may increase or decrease in response to economic and financial events (whether real, expected or perceived) in the U.S. and global markets. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of debt securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. As interest rates rise, the value of certain income investments is likely to decline.

Henry Mason is an ESG senior research associate for Calvert Research and Management, which specializes in responsible and sustainable investing across global capital markets. He is responsible for evaluating sustainable fixed income, as well as supporting environmental, social and governance (ESG) research coverage of the electrical equipment industry. He joined Calvert in 2019.

Henry began his career in the investment management industry in 2019. Before joining Calvert, he was a climate change and sustainability specialist at ICF, a global management consulting firm. Previously, he served as a research fellow at the National Center for Environmental Economics, an office of the EPA, where he conducted quantitative econometric research to support rulemaking.

Henry earned a B.A. as well as an M.E.S. from the University of Pennsylvania.

Brian Ellis is a vice president and portfolio manager for Calvert Research and Management, which specializes in responsible and sustainable investing across global capital markets. He joined Calvert Research and Management in 2016.

Brian began his career in the investment management industry in 2006. He has been affiliated with the Eaton Vance organization since 2016. Before joining the Eaton Vance organization, he was a portfolio manager of fixed-income strategies for Calvert Investments. Previously, he was a software engineer and analyst at Legg Mason Capital Management (now ClearBridge Investments).

Brian earned a B.S. in finance from Salisbury University. He is a CFA charterholder and an FSA credential holder. He is a member of the CFA Institute and the CFA Society of Boston.

This easy-to-follow five-step guide assists retirement plan sponsors considering the addition of investment options that address environmental, social and governance (ESG) criteria to their defined contribution (DC) retirement plans. The five steps include increasing plan sponsor knowledge of sustainable investing, gauging participants’ interest, discussing implementation, choosing funds and educating participants. It also contains a summary of studies on the financial performance of funds utilizing ESG criteria as well as updates on relevant Department of Labor regulations. Along with practical tips and suggestions, the guide lists links to additional resources.

This easy-to-follow five-step guide assists retirement plan sponsors considering the addition of investment options that address environmental, social and governance (ESG) criteria to their defined contribution (DC) retirement plans. The five steps include increasing plan sponsor knowledge of sustainable investing, gauging participants’ interest, discussing implementation, choosing funds and educating participants. It also contains a summary of studies on the financial performance of funds utilizing ESG criteria as well as updates on relevant Department of Labor regulations. Along with practical tips and suggestions, the guide lists links to additional resources.

The green bond market is on fire, channeling record funds into climate-friendly projects around the globe — and at a relatively low cost to issuers. Green bonds offer a promising synergy between investors with trillions of dollars chasing ESG products and the need for climate finance, especially in developing countries where access to affordable debt is essential to install those solar arrays, wind turbines and other infrastructure to underpin a new green economy.

The green bond market is on fire, channeling record funds into climate-friendly projects around the globe — and at a relatively low cost to issuers. Green bonds offer a promising synergy between investors with trillions of dollars chasing ESG products and the need for climate finance, especially in developing countries where access to affordable debt is essential to install those solar arrays, wind turbines and other infrastructure to underpin a new green economy.

Green bonds help finance environmental and climate change mitigation projects around the world, and they’re already proven to be an effective way to mobilize private capital. They have the same fundamental risk and return characteristics as conventional bonds, and investors may not need to sacrifice yield or assume additional risk to add these fixed income options to their portfolios.

Green bonds help finance environmental and climate change mitigation projects around the world, and they’re already proven to be an effective way to mobilize private capital. They have the same fundamental risk and return characteristics as conventional bonds, and investors may not need to sacrifice yield or assume additional risk to add these fixed income options to their portfolios.

Wind turbine image courtesy of Praxis Mutual Funds

Wind turbine image courtesy of Praxis Mutual Funds

My book, Investing in a New Climate is not about doom and gloom, but about adapting to change. Climate change is about the shifting of circumstances we have long taken for granted. To survive — and succeed — we must adapt. We must learn how to live and how to plan ahead within the realm of reasonable extrapolation of a changing global climate. Warming of the climate system is unequivocal and, since the 1950s, many of the observed changes are unprecedented. The atmosphere and oceans have warmed, the amounts of snow and ice have diminished, the sea level has risen, and the concentration of greenhouse gases has increased.

My book, Investing in a New Climate is not about doom and gloom, but about adapting to change. Climate change is about the shifting of circumstances we have long taken for granted. To survive — and succeed — we must adapt. We must learn how to live and how to plan ahead within the realm of reasonable extrapolation of a changing global climate. Warming of the climate system is unequivocal and, since the 1950s, many of the observed changes are unprecedented. The atmosphere and oceans have warmed, the amounts of snow and ice have diminished, the sea level has risen, and the concentration of greenhouse gases has increased.