Regeneration: Ending the Climate Crisis in One Generation

From the NYT bestselling creator of “Drawdown” and one of the environmental movement’s leading voices comes a radical new understanding of and practical approach to climate change.

The dangers of a warming world have been in the public eye for at least the last fifty years, and yet it wasn’t until 2016 that 191 countries came together to sign the Paris Agreement, committing to prevent global warming from exceeding 1.5 degrees centigrade. Only two countries have targets consistent with that goal, and G7 countries do not even come close. The most asked questions by people are: What can I do? Where do I start? And how can I make a difference? When people see what climate change is doing to the earth, they can feel overwhelmed, anxious, confused, or very small — “I am just one person.”

The dangers of a warming world have been in the public eye for at least the last fifty years, and yet it wasn’t until 2016 that 191 countries came together to sign the Paris Agreement, committing to prevent global warming from exceeding 1.5 degrees centigrade. Only two countries have targets consistent with that goal, and G7 countries do not even come close. The most asked questions by people are: What can I do? Where do I start? And how can I make a difference? When people see what climate change is doing to the earth, they can feel overwhelmed, anxious, confused, or very small — “I am just one person.”

Enter environmentalist, entrepreneur, and activist Paul Hawken. A leading voice in the climate movement, Hawken has dedicated his life to environmental sustainability and to changing the relationship between business, society, and the environment. His eight books include the 2017 New York Times bestseller Drawdown, which Outside Magazine called “a bold plan to beat back climate change.” This fall, Hawken returns with Regeneration: Ending the Climate Crisis in One Generation (Penguin Books; September 2021). An urgent and, ultimately, hopeful work — launched in conjunction with his Regeneration organization — Regeneration weaves justice, climate, biodiversity, equity, and human dignity into a seamless tapestry of action, policy, and transformation. It is the first book to describe and define the burgeoning regeneration movement spreading rapidly throughout the world — an inclusive and multifaceted undertaking that aims to end the climate crisis in one generation. As Jane Goodall writes in her foreword, “Regeneration is a rebuttal to doomsayers who believe it is too late.”

In Regeneration, Hawken states:

- To reverse the climate crisis, the majority of humanity needs to be engaged. 98% of the world is not.

- To get the attention of humanity, humanity needs to feel it is getting attention.

- To save the world from the threat of global warming, we need to create a world worth saving.

- To succeed, climate solutions must directly serve our children, the poor, and the excluded.

- This means we must address current human needs, not future existential threats, real as they are.

In order to do this, Hawken identifies six basic frameworks to solve the climate crisis in Regeneration:

- Equity: Equity encompasses everything. All that needs to be done must be infused by equity. Fairness is about how we treat one another, ourselves, and the living world. We have transformed the planet in a geological blink of an eye. Transforming the climate crisis means mending the vital relationships and understandings between people, reconnecting humanity and nature, and restoring nature itself.

- Reduce: The best method of ending global greenhouse gas emissions is simple: don’t put them into the atmosphere. It is also the most difficult, while being the greatest economic opportunity in history. Hawken predicts the end of fossil fuels by 2040 and the advent of totally electrified world by 2050.

- Protect: The world’s terrestrial ecosystems contain four times more carbon than the atmosphere. If we lose just 6 percent of our grasslands, forests, mangroves, seagrasses and wetlands, we will see a 100 ppm increase in atmospheric carbon dioxide. Protecting wildlife corridors, bioregions, biomes, and all the forms of life within them are crucial to stopping the climate crisis.

- Sequester: This means bringing carbon back home. It is the nutrient required by life to regenerate the earth. The primary way to sequester carbon is through regenerative agriculture, grazing ecology, proforestation, afforestation, degraded land restoration, and protecting existing ecosystems.

- Influence: Laws, bureaucratic regulations, perverse subsidies, bygone policies, and outmoded building codes often obstruct climate initiatives. Making our voices heard requires letters, emails, protests, boycotts, and lobbying legislators, companies, city council members, and corporate CEOs.

- Support: Regeneration contains links to a vast network of organizations, ideas, groups, videos, books, and people who are implementing regeneration worldwide.

Hawken explains how Regeneration creates abundance, not scarcity. It expands what is possible. It is about the optimism of action instead of the pessimism of thought. Regeneration is an inspiring and necessary guide to today’s climate movement that will enable readers to understand its many facets — and more importantly, to act.

Paul, in his usual inimitable way, describes the most important solutions to the environmental and social problems we have brought upon ourselves, and shows how they are inseparably linked. Regeneration is honest and informative, a rebuttal to doomsayers who believe it is too late. He echoes my sincere belief that we have a window of time, that there are practical solutions, and that we and all our institutions can initiate and implement them in order to restore life climatic stability and on Earth. Let us work to live up to our scientific name: Homo sapiens, the wise ape.

— From the Foreword by Jane Goodall

Find out more at the Regeneration website which is the world’s largest, most complete listing and network of solutions to the climate crisis.

About the Author: Paul Hawken is an environmentalist, entrepreneur, author and activist who has dedicated his life to environmental sustainability and changing the relationship between business and the environment. He is one of the environmental movement’s leading voices, and a pioneering architect of corporate reform with respect to ecological practices. He is the bestselling author of eight books that have been published in 30 languages in more than 50 countries and have sold more than 2 million copies, as well as dozens of articles, op-eds, and other papers concerning the environment, the ethical responsibility of business, and social justice. Hawken is a renowned lecturer who has keynoted conferences and led workshops on the impact of commerce upon the environment, and consulted with governments and corporations throughout the world.

Additional Articles, Energy & Climate, Food & Farming, Impact Investing, Sustainable Business

Report Highlights Include:

Report Highlights Include:

With so many investment options geared towards ESG strategies, it can be hard to identify ones that drive direct and measurable impact towards their desired cause. The investments that can trace their value to an actual effect are said to have “additionality.” For example, buying the stock of the even the best-intentioned company that is already publicly listed does not create additionality, but investing with a firm that builds new distributed scale sustainable infrastructure projects does. Each dollar is directed into building a real asset, which creates jobs, injects money into local communities, and produces quantifiable ecological impacts that positively impact all socioeconomic strata.

With so many investment options geared towards ESG strategies, it can be hard to identify ones that drive direct and measurable impact towards their desired cause. The investments that can trace their value to an actual effect are said to have “additionality.” For example, buying the stock of the even the best-intentioned company that is already publicly listed does not create additionality, but investing with a firm that builds new distributed scale sustainable infrastructure projects does. Each dollar is directed into building a real asset, which creates jobs, injects money into local communities, and produces quantifiable ecological impacts that positively impact all socioeconomic strata.

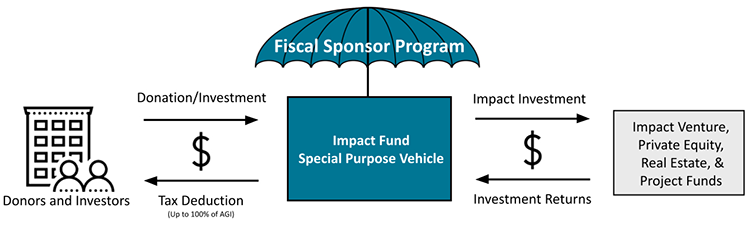

Fundraising for traditional investment funds is trying under the best of circumstances. The degree of difficulty for social and environmental impact funds seeking investment during uncertain times can be far higher. Nonetheless, there are innovative, albeit less traveled, paths to investment that may be well suited for impact funds.

Fundraising for traditional investment funds is trying under the best of circumstances. The degree of difficulty for social and environmental impact funds seeking investment during uncertain times can be far higher. Nonetheless, there are innovative, albeit less traveled, paths to investment that may be well suited for impact funds.

Contrary to popular belief,

Contrary to popular belief,

Put another way, ownership capitalizes on the power of buying a home by converting a portion of what would otherwise be 100 percent consumer spending (renting) into a combination of consumer spending and investment. And it does so without additional resources. The home buying investment simply converts some portion of an existing expense (renting) into an investment in real estate.

Put another way, ownership capitalizes on the power of buying a home by converting a portion of what would otherwise be 100 percent consumer spending (renting) into a combination of consumer spending and investment. And it does so without additional resources. The home buying investment simply converts some portion of an existing expense (renting) into an investment in real estate.

Nicole Middleton Holloway: Community investing is an investment in a targeted community based on impact and need. It is typically an investment that doesn’t have market rate rates of return, because the point of the investment is to uplift a certain community need. It can be for a variety of different areas, from funding entrepreneurs and micro enterprises and other small businesses to focusing on specific communities, like low income, BIPOC (Black, Indigenous and People of Color) communities. It can be focused on healthy food systems, affordable housing, or wherever there’s a need. The investment can be an investment note or a CD, which is something that we, at Natural Investments do quite often through places like Self Help Credit Union or Hope Credit Union.

Nicole Middleton Holloway: Community investing is an investment in a targeted community based on impact and need. It is typically an investment that doesn’t have market rate rates of return, because the point of the investment is to uplift a certain community need. It can be for a variety of different areas, from funding entrepreneurs and micro enterprises and other small businesses to focusing on specific communities, like low income, BIPOC (Black, Indigenous and People of Color) communities. It can be focused on healthy food systems, affordable housing, or wherever there’s a need. The investment can be an investment note or a CD, which is something that we, at Natural Investments do quite often through places like Self Help Credit Union or Hope Credit Union.

Community Capital Management, LLC (CCM), a leading impact and environmental, social, and governance (ESG) investing manager, recently released a new report, “Aligning Faith and Finance”.

Community Capital Management, LLC (CCM), a leading impact and environmental, social, and governance (ESG) investing manager, recently released a new report, “Aligning Faith and Finance”.

Impax Asset Management is celebrating the 50th birthday of the

Impax Asset Management is celebrating the 50th birthday of the