Blue Foundry Events virtually connects the global stakeholder community to drive engagement and share knowledge to solve wicked water challenges

Water Foundry, a global advisor in solving “wicked water” challenges and driving technology innovation, and ConnectMii, a company and platform that delivers unique virtual conference experiences, recently announced the launch of Blue Foundry Events, a virtual meeting and events platform that aims to facilitate meaningful engagement amongst water industry stakeholders.

During this period of remote-only business where meetings and conferences have shifted almost entirely online, Blue Foundry Events provides a platform to mobilize entrepreneurs, investors, non-governmental organizations, the public sector, businesses, solution providers, academics and civil society to solve challenges both local and global related to water quantity, water quality and access to sanitation and hygiene.

“The ability to seamlessly gather remotely has never been more critical than it is now,”said Will Sarni, Founder and CEO of Water Foundry and co-founder of Blue Foundry Events. “With this new normal being the way forward for the foreseeable future, we cannot neglect the need to still bring together the global water community to continue the important work underway to solve wicked water problems. Blue Foundry Events is our answer to how we stay the course during these times and beyond.”

Blue Foundry Events will be held on ConnectMii’s proprietary Virtual Conference Experience (VCX) virtual event platform. VCX incorporates live and pre-recorded video streaming and live audience interaction into a familiar guidebook format that serves as a promotional brochure, an event staging platform and a post-event archive. Participating organizations can take advantage of the VCX guidebook interactivity to connect visitors to their site and allow visitors to book scheduled private one-on-one video meetings.

ConnectMii’s CEO Mark Barounos said, “ConnectMii is excited to be working with Water Foundry to bring Blue Foundry Events to the public. We originally entered the virtual event space in 2010 in connection with an event focusing on sustainable business practices where the use of video technologies was itself a prime example of sustainability in action. Having spent the last 10 years helping to develop the virtual event industry, it is gratifying to put that experience to work in the water education sector.”

Water Foundry creates leading edge water strategies for US and non-US multinationals, non-governmental organizations, investors and the public sector. These strategies range from initial water strategy efforts to moving companies to more advanced water stewardship strategies and validating program performance. The company also works with innovative water technology startups and growth stage companies as an advisor on business strategy, funding and business development. Water Foundry was founded by Will Sarni, an internationally recognized thought leader on water strategy and innovation. Learn more at www.waterfoundry.com.

About ConnectMii

ConnectMii is a Colorado-based industry pioneer in the virtual event management space. The company produces and manages video-enabled events under its own banner and on behalf of corporate, government and association clients, for industries as wide-ranging as sustainability to geospatial to energy to retail. ConnectMii is platform-agnostic, and has held events on numerous virtual event platforms, in addition to its Virtual Conference Experience (VCX) solution.

Apple has released a 10-year roadmap to ensure that every device it produces has a net-zero climate impact by 2030, as part of its plans to become carbon neutral.

The company announced recently its commitment to achieving a net-zero carbon footprint across its product life cycles and manufacturing supply chains in 10 years’ time.

Apple said its global corporate operations are already carbon neutral but plans for its entire business, including all of its devices, to have a net-zero climate impact by 2030.

Outlined in its 2020 Environmental Progress Report, the goal is to reduce its emissions by 75 per cent and to develop carbon removal solutions for the remaining 25 per cent to create a net zero sum.

“Climate action can be the foundation for a new era of innovative potential, job creation, and durable economic growth,” said Apple’s CEO Tim Cook.“With our commitment to carbon neutrality, we hope to be a ripple in the pond that creates a much larger change.”

Apple’s plan to become carbon neutral by 2030 involves using renewable energy.

Apple Publishes 10-year Climate Roadmap

Apple has created a 10-year climate roadmap as part of its report, which details the interventions and changes it intends to make by 2030.

The measures are developed around five pillars: low-carbon design, energy efficiency, renewable electricity, direct emissions abatement and carbon removal.

As part of its plan to create low carbon products, Apple is developing a carbon-free aluminium smelting process that releases oxygen instead of greenhouse gases. It is currently working with aluminium suppliers to create the new production method, which it claims is the first of its kind.

The first batch of this low-carbon aluminium is currently being used to produce a 16-inch MacBook Pro.

“The innovations powering our environmental journey are not only good for the planet – they’ve helped us make our products more energy-efficient and bring new sources of clean energy online around the world,” Cook said.

Read the full Dezeen article written by Bridget Cogley which includes Apple’s plans to develop renewable power plants.

The world’s leading climate scientists have warned that we have only a few years left to keep global warming below 1.5°C, beyond which even half a degree more will significantly worsen the risks of drought, floods, extreme heat and poverty for hundreds of millions of people. To help guide policy making and discussion around the world, the IPCC has issued regular reports since 1988 drawing upon carefully constructed scenarios to predict the likely path of greenhouse-gas emissions and the resulting rise in global temperatures. The proposed scenarios must take into account not only complex scientific and environmental factors but also projections of population, economic growth, technology, and government policies.

For its Fifth Assessment Report, released in 2014, the panel collected a broad and numerous collections of possible scenarios, dubbed “representative concentration pathways” (RCPs) and selected four for deeper analysis. The most serious, RCP 8.5, is often called “business-as-usual” because it assumes no changes in government policies. To meet the recommended 1.5°C target will require emissions not just to stabilize but to decrease significantly. This would require drastic and immediate transformation of our human infrastructure, including how we generate energy and fuel our economy (IEA 2020).

Whether COVID-19 changes our collective mindset and lowers future emissions trajectories depends on whether it changes the path of the economy and investments in fossil-fuel usage or policy, moving beyond the business-as-usual scenario and introducing new measures such as carbon taxation. To date, reductions (Liu et al 2020) in emissions over the pandemic have yet to produce a perceptible change in concentrations, which are what affect climate as this years’ emissions come on top of century’s accumulated emissions. Though the economic consequences of locking down to quell the spread of the coronavirus will potentially eliminate many companies, it may also thwart the fast expansion of new infrastructure or renewable energy development aimed at reducing resource dependency. One interesting question to address now is how the overall growth trajectory of renewables will be impacted by this pandemic?

According to managers responding to Pensions & Investments’ annual survey, U.S. institutional energy assets totaled $1.8 billion as of Dec. 31, 2019 down 35.2% from a year earlier and 43% from Dec. 31, 2014. Energy investments have been hit by a double whammy this year that includes falling oil prices with domestic crude prices falling to below zero in April, making renewables less competitive, and a worsening economic outlook due to the global pandemic. At the same time, energy managers are expected to invest more in renewables. Most investors expect that the rollout of renewable energy will continue and even accelerate.

Additionally, in the electricity sector, demand has been significantly reduced as a result of lockdown measures, with knock-on effects on the power mix. Electricity demand has been depressed by 20 percent or more during periods of full lockdown in several countries, as upticks for residential demand are far outweighed by reductions in commercial and industrial operations. Demand reductions have lifted the share of renewables in the electricity supply, as their output is largely unaffected by demand. For the year as a whole, output from renewable sources is expected to increase because of low operating costs and preferential access to many power systems. This would mean that low-carbon sources far outstrip coal-fired generation globally, extending the lead established in 2019 (World Energy Investment 2020).

With increased capital investments in the renewable sector and higher representation of renewables in the electric sector, the path to a low-carbon future has become more desirable but uncertain as well. World leaders are now faced with a choice: Reopen economies powered by the failing fuel sources of the past, or jump-start paths toward a clean, secure and prosperous future by investing now for the long term. The bigger question is whether the expansion of renewables is sufficient to achieve the recommended 1.5°C target temperature?

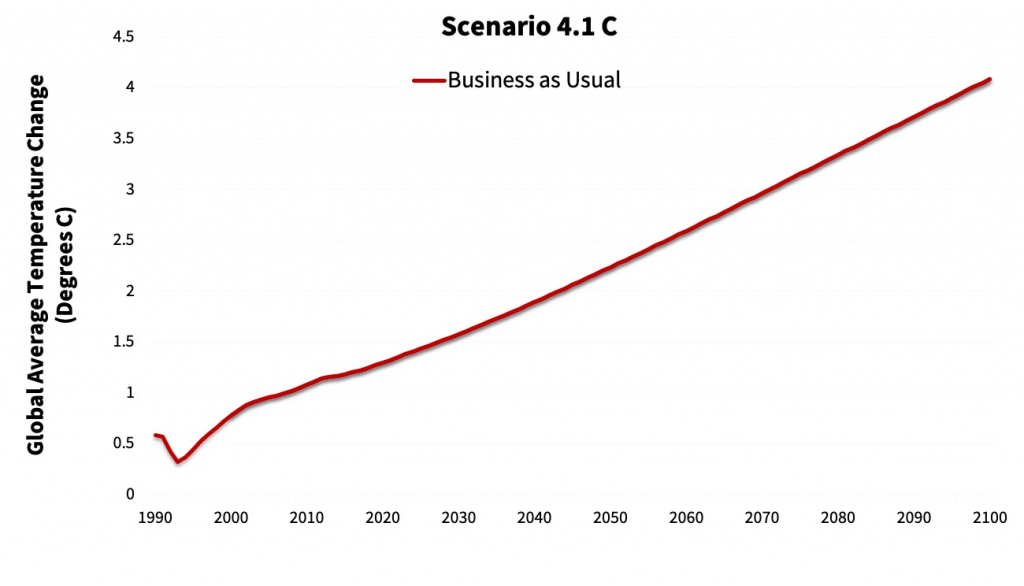

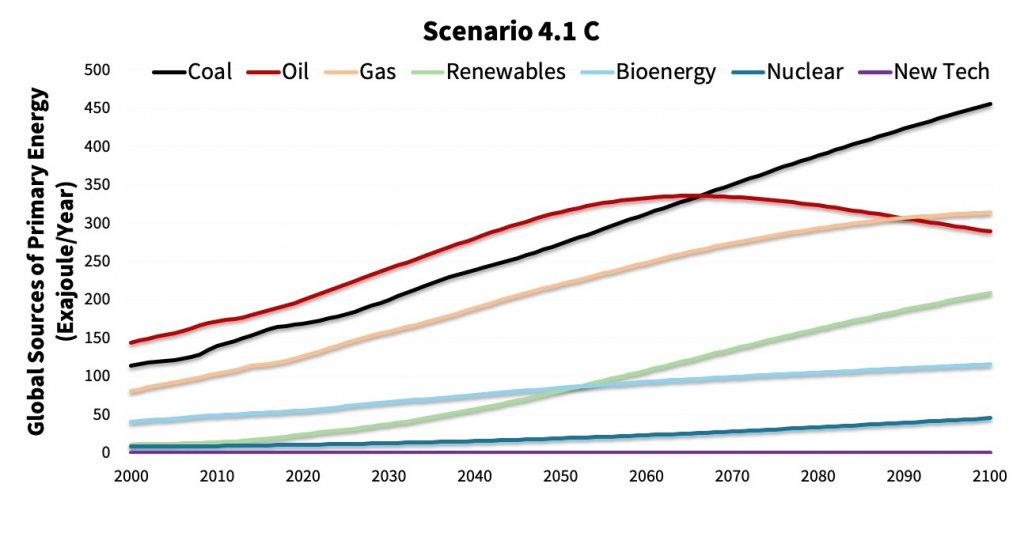

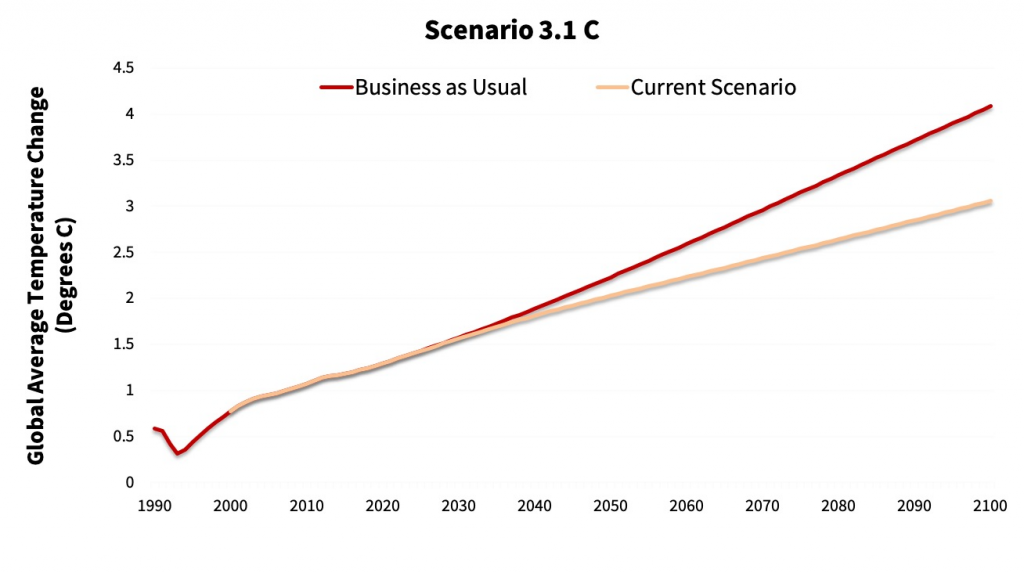

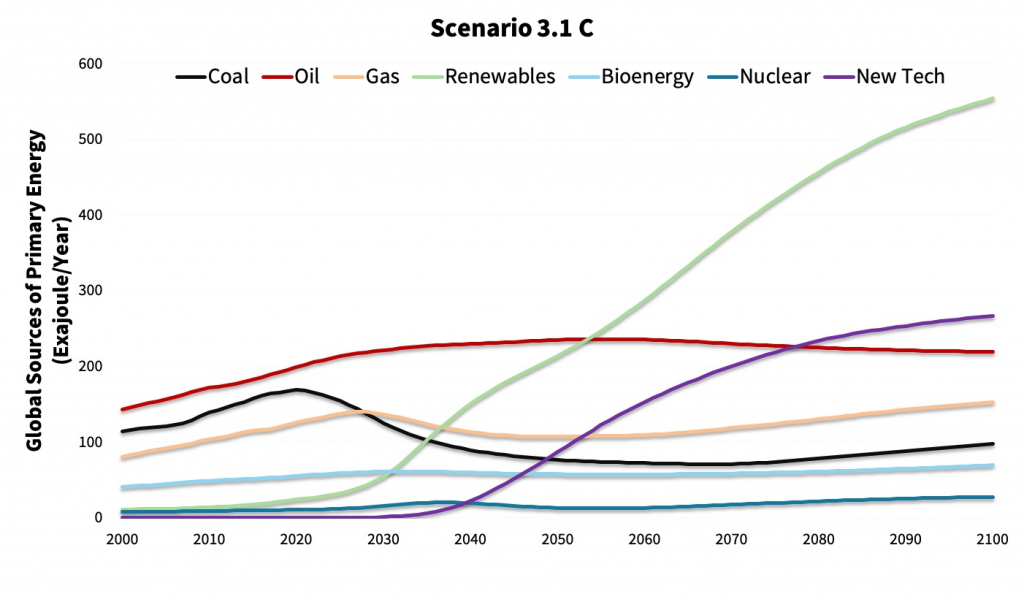

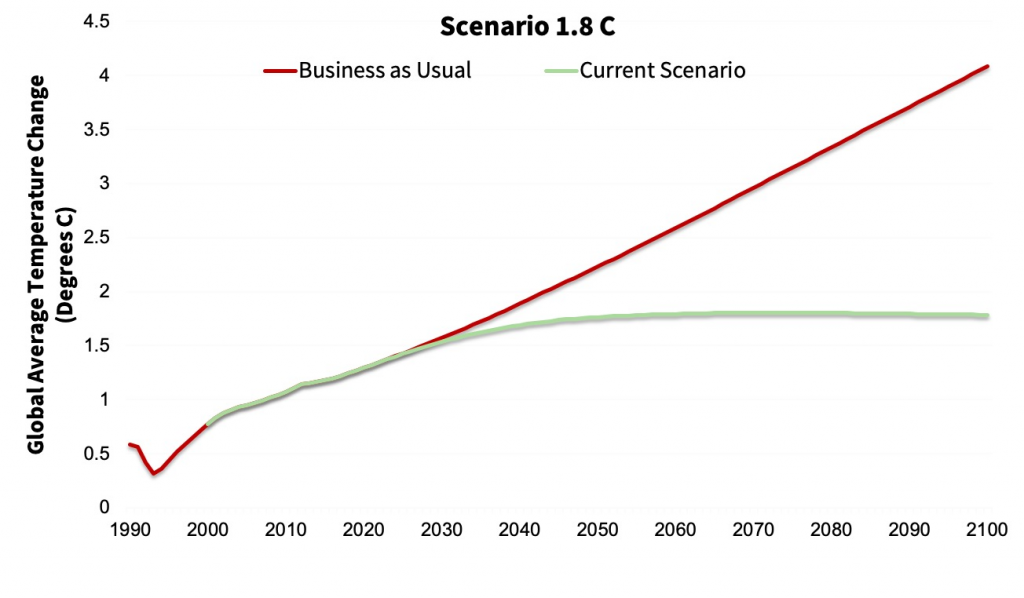

We use a scientific, credible, freely available policy simulation model to scientifically answer the question above. We observed that policy changes focused on highly subsidizing renewables, imposing a very high tax on carbon and even allowing for huge technological breakthroughs are insufficient to bend the global temperature curve from current business-as-usual to the recommended 1.5°C target temperature. These renewable energy focused changes will help us only to slow down global warming by 1.0°C (from current 4.1°C to 3.1°C) (Figure 1 and Figure 2).

Figure 1– Business-as-Usual Scenario 4.1 C. No changes in energy supply, transport, building and industry, land and industry emissions, carbon removal. Source: EN-ROADS

Figure 2– Scenario 3.1 C. Renewable energy highly subsidized, very high carbon tax, huge technological breakthrough. Source: EN-ROADS

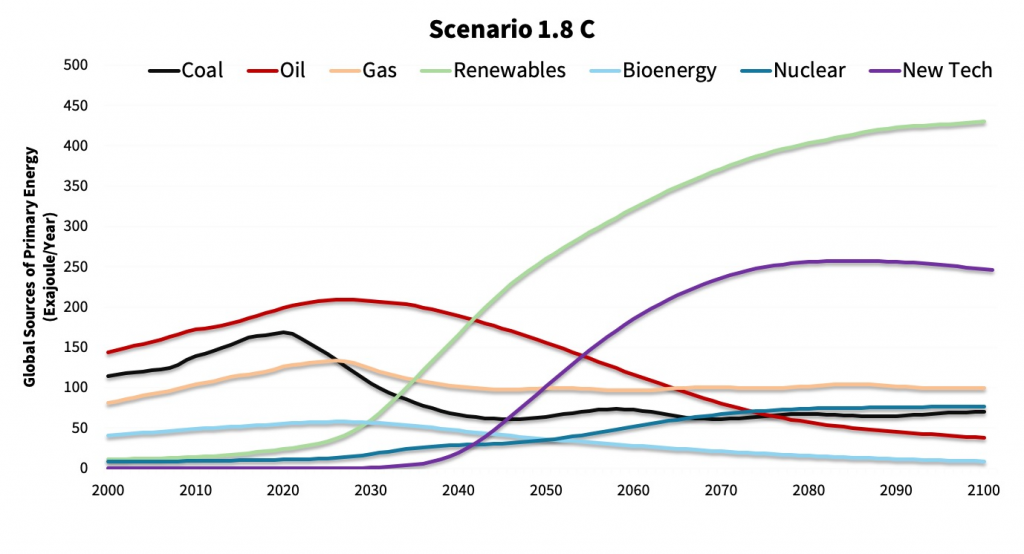

To further bend the temperature curve, policy makers, investors and corporations need to do two things. First is to focus on increased energy efficiency and electrification in transport, building and other sectors. Second, is that more attention needs to be given to new technologies that help to reduce emissions or reduce the impact of emissions from existing energy infrastructure. This could include agricultural practices that sequester carbon in soils, bioenergy with carbon capture and storage, direct air capture and potentially geoengineering solutions such as stratospheric aerosol injection, marine cloud brightening, cirrus cloud thinning, or ground-based albedo modification (Figure 3).

Figure 3– Scenario 1.8 C. A Cross-sectoral transformation is needed to hit the Paris Agreement goal. Changes in energy industry: highly subsidized renewable energy, very high carbon tax, huge technological breakthrough. Changes in transport, buildings and industry: energy efficiency highly increased as well as electrification incentivized. Changes in land and industry emissions: Highly reduced deforestation, moderately reduced methane & others. Changes in carbon removal: medium growth in technology. Source: EN-ROADS

Additionally, globally we need to increase the development and application of reporting metrices and standards that are focused on measuring emissions reductions (for all GHG emissions including carbon and methane). Organizations leading the climate reporting disclosures such as Task Force on Climate-related Financial Disclosures (TCFD) must include carbon reduction reporting in addition to carbon foot-print disclosures. Carbon reduction reporting is a key practice that Entelligent, a data platform company based in Boulder, Colorado, recommends for its large institutional clients.

Advancing energy efficiency and direct desired policy shocks such as high subsidies to renewables and a carbon tax will trigger huge shifts in corporate balance-sheets. If there is global desire to bend the temperate curve to the 1.5°C target, financial stakeholders such as banks, asset managers, institutional investors, pension funds and portfolio managers must take action and integrate knowledge and information on climate transition risk with their investment strategies.

The policy, supply chain and energy mix disruption shocks that we are experiencing related to COVID-19 are classified the same as climate change — as an unpredictable unknown. Accelerating change and bending the temperature change curve demands that we immediately account for such shocks by accounting for climate change risk.

Article by Pooja Khosla Ph.D., Vice President Client Development at Entelligent. Dr. Khosla is an economist, econometrician, and mathematician who has deep knowledge to build investing solutions. She has extensive experience in predictive modeling, microfinance and designing impact investment tools. Khosla has been working on impact solutions since 2003 both nationally and internationally. Khosla has been working with Entelligent since 2016 developing Entelligent’s data science team, Smart Climate technology, Smart Climate Indices as well as additional climate risk related products. She is one of the inventors of patented Smart Climate technology. Khosla has several publications in economics, impact investing and microfinance. Besides designing sustainability products Khosla has an active teaching career training student in economic applications and data science. Khosla holds a Ph.D in economics, and master degrees/diploma in three disciplines including economics, statistics and public relations.

References

Liu Z, Deng Z, Ciais P, Lei R, Feng S, Davis SJ, Wang Y, Yue X, Lei Y, Zhou H, Cai Z. Decreases in global CO $ _2 $ emissions due to COVID-19 pandemic. arXiv preprint arXiv:2004.13614. 2020 Apr 28.

Financial Stability Board 2016. Recommendations of the Task Force on Climate-related Financial Disclosures. Financial Stability Board, Basel, Switzerland (2016).

Located on the “quiet side” of Maine’s Mount Desert Island, Tremont is a fishing town with a significant influx of summer tourism in typical years, thanks to nearby Acadia National Park. While the town is small, with only 1,529 year-round residents, its leadership values using natural resources sustainably. So, when the town was looking for ways to reduce the fiscal and environmental costs of its energy needs, it made sense to look to solar.

At the time of the Tremont solar installation, in early 2019, Maine was not yet a “solar-friendly state.” The policies on the books didn’t provide the regulatory predictability developers desired and Maine was last among New England state in solar energy development and solar job creation. But that didn’t stop Tremont from pushing forward with the installation of a new array on the town’s capped landfill. Now operational, the array generates 100 percent of the electricity needed for the town’s municipal buildings.

Because solar development was relatively uncommon in the state at the time, it took a unique partnership between a local solar installer, The Nature Conservancy of Maine and community development financial organization (CDFI), Coastal Enterprises, Inc. (CEI), to make it happen. The Nature Conservancy provided a grant to CEI that lowered the total cost of the loan. The partnership worked together to develop a power purchase agreement (PPA) financing structure that allowed Tremont to purchase the array with no upfront cost and a fixed six-year electricity purchase rate that is lower and more predictable than their previous grid-based costs.

“This solar project is a win-win for the community,” said Tremont Town Manager Christopher Saunders. “It lowers the town’s long-term energy costs and is good for the environment.”

Tremont Solar, Tremont, Maine

In June 2019, just months after the Tremont array went live, state legislators passed new legislation that encouraged both grid-scale and distributed solar, and suddenly the future for solar in Maine was a lot brighter. As municipal managers like Tremont’s Saunders shared their positive experiences with solar arrays with their peers in other communities, interest in municipal installations increased. However, since the legislative shift incentivizing entry to the market was so new, local banks weren’t familiar with the financial structures.

CEI’s mission is to grow good jobs, expand environmentally sustainable enterprises, and increase more broadly shared prosperity in Maine and other rural regions. CDFIs, including CEI, develop a deep connection to the communities where they do business, which translates into a willingness and commitment to one-on-one technical assistance and specialized programs that are often too time-consuming or costly for mainstream financial institutions to consider. Often, CDFIs demonstrate proof of concept and demand for a new financial product, which serves as a catalyst for investment from more traditional lenders. In the words of John Egan, CEI’s Chief Investment Officer, “We take the sharp edges off the new stuff and bring it more mainstream.”

To expand municipal solar in Maine, this has meant helping interested community banks learn the ropes through participation in a CEI municipal solar loan. CEI takes the lead in organizing, negotiating and documenting a solar financing transaction, while the community bank provides funding dollars and, in the process, learns how to replicate the model on their own. The involvement of community banks, along with the changes in legislation, has allowed the scale of projects to expand across rural Maine, often bundling multiple communities as solar energy off takers (or purchasers) – a move that increases adoption of solar technology across the state and allows everyone to benefit from economies of scale.

Communities of all sizes across Maine are taking advantage of the new solar environment and demand shows no sign of slowing down, even in the current COVID-19 pandemic. Municipal leadership and their communities continue to seek the environmental and financial benefits of renewable energy; the state is developing plans to make Maine carbon-neutral by 2045. While the benefit of lower-rate and fixed, rather than variable, electricity costs continues to make financial sense for municipalities. The savings to the municipality can either be passed on to taxpayers or utilized to support services and programs, a valuable opportunity as communities deal with extra costs and support demands due to the pandemic.

Rob Martin pulls conduit to the 192 solar panels installed by Insource Renewables atop a cow barn at the Milkhouse in Monmouth. The array is expected generate 72 kilowatts directly into the grid through an upgraded electrical panel of 400 amps. The sun harvesting equipment utilized to defray the cost of milking and manufacturing organic yogurt was purchased in part through a Rural Energy for America Program renewable energy grant administered the US Department of Agriculture, according to farmer Andrew Smith, which supplemented a grant from Androscoggin Council of Governments. Staff photo by Andy Molloy

On the supply side, the logistics of solar installation allow employees to continue to work safely under social distancing guidelines and some local installers are nearing capacity, offering the promise of future job creation in addition to the fiscal and environmental benefits. CEI has led 11 municipal solar financings in the last two years, representing over $6,000,000 in total loans provided within that time frame. The community profiles are as varied as Freeport, a popular tourist destination and city of 8,000 in southern Maine, and Caribou, a town of about 1,800 that is less than 12 miles from the Canadian border.

“The inspiring part of this work is when rural Maine communities recognize solar power as not only good environmental stewardship, but also an economic gain,” Egan added. “Now that the arrays are on town land, renewable energy generation goes from an abstract concept to something everyone can see and spark conversation. As investors, we demonstrate that renewable energy is for everyone, not just for wealthy communities.”

Jan and Rob Goranson installed solar trackers on their certified Organic, Goranson Farm offseting nearly 90% of the farm’s considerable electric bill – Dresden, Maine

As more communities and traditional lenders tackle municipal solar financing in the state, CEI is already looking toward the next opportunity to expand access to financing for solar installation in Maine. In addition to one-off installations with businesses and farms, CEI is developing a model for Resident Owned Communities (ROCs), manufactured housing neighborhoods owned and governed by the residents that work in ways similar to a mini municipality. CEI is in the process of identifying a ROC to serve as this model’s Tremont, the community that will prove the benefits of solar for its residents and, if successful, act as the first domino in a chain of solar electricity adoption benefiting similar communities across the state.

Article by Leah B. Thibault, Marketing Manager for Coastal Enterprises, Inc. Leah manages marketing and communications initiatives at CEI, with a focus on storytelling. As a writer, her work has appeared in GreenMoney Journal, Triple Pundit, Food Industry Executive, USDA Rural Cooperatives Magazine and Taproot Magazine. In addition to her work at CEI, Leah runs a small business as a craft pattern designer and previously worked in the nonprofit performing arts and educational sectors. Leah holds a B.A. from Willamette University in Salem, Oregon.

Data centers have made significant investments in energy efficiency, but our insatiable appetite for data continues to grow. Renewable energy can reduce our data’s carbon footprint.

Buildings consume 40 percent of global energy and create 30 percent of global energy-related greenhouse gas emissions; they are a big part of the climate change puzzle.[1] Energy heats and cools our buildings and it keeps the lights on. Obvious energy reduction strategies are better insulation, LED lighting, and smart thermostats. The energy needs of our data, and the solutions, are less obvious. We’ve moved our music, our movies, and more of our lives into the “cloud”. But our data isn’t actually stored in a cloud. It resides in real buildings we call data centers, which have a large and growing carbon footprint.

Data centers now use over one percent of global electricity. And because the internet never shuts off, power is required 24 hours a day, seven days a week. Using so much global energy puts a spotlight on what types of energy is being used at technology companies and the data centers that house internet services across the globe.

In 2010, the advocacy organization Greenpeace campaigned for technology companies to use more renewable energy. Their “Clicking Clean” program initially gave many tech firms low scores.[2] Leading brands like Google, Apple, Microsoft, and Salesforce began making commitments to switch to renewables. And data centers, who provide many of the storage, routing, and networking functions for the big tech firms, started figuring out how to give their customers what they want.

The Path to Renewable Energy

Reducing Energy Use Through Efficiency – Ten years ago, data centers consumed 100 to 200 times more energy more than similar sized buildings.[3] Fortunately, companies recognized that “nega-watts”- the electricity they don’t consume – are both the cleanest and the cheapest energy available. Data centers have made massive gains in efficiency through processor-efficiency improvements and reductions in idle power. These technological advances help servers process 550 percent more data for only six percent more energy.[4] Incremental efficiency improvements can only get us so far when our demands for data continue to grow exponentially. Vert looks for companies that are innovating ways to switch to renewables. Five REITs discussed below are holdings in the Vert Global Sustainable Real Estate Fund: Prologis 4.88 percent, Macerich 0.07 percent, Iron Mountain 1.18 percent, Equinix 4.99 percent and Digital Realty 4.60 percent as of May 31, 2020.

Interior of Equinix IBX data center DC12, Washington D.C

On-Site Renewable Energy Production – Some building types can make excellent use of their large flat roofs to deploy solar panels. Prologis, the world’s largest warehouse REIT (pictured at top), is also one of the largest installers of solar panels. Prologis roof-top solar currently generates 165 Megawatts which is enough to power 24,484 homes for a year.[5] Big box retailers like Walmart and Target have ample roof space and are among the top five producers of roof-top solar energy in the US. Retail real estate, like Macerich REIT who own several sprawling malls in Los Angeles, have deployed large solar arrays on their mall rooftops. But for many other building types this isn’t possible.

Data centers use more energy than is practical to generate onsite. There is no way to fit enough solar panels on the roof to generate enough power to drive all the servers and air conditioners required. Iron Mountain recently installed the largest on-site solar on a datacenter in the US, a 7.2 Megawatt system in Edison, New Jersey. It only powers 15 percent of the building’s energy needs.[6]

Purchase Renewable Energy – Today, if you want to purchase renewable energy, your options largely depend on who your local utility is. For instance, coal-fired power plants generate 25.4 percent of electricity in Texas, 3.8 percent in Virginia, and only 0.1 percent in California.[7] Renewable energy sources made up 35 percent in California, 16.1 percent in Texas and 8.5 percent in Virginia. If you are in Loudoun County, Virginia, the home to the highest concentration of data centers in the world, you don’t have good options. The local utility provider, Dominion Virginia Power, relies heavily on fossil fuels and has historically been resistant to switch its fuel mix to renewables.

Power Purchase Agreements – Data centers wanting a greener energy profile, but who are stuck with local utilities providing brown energy, need to get creative.

In 2015, Equinix completed a Power Purchase Agreement (PPA) with renewable energy firms NextEra Energy and Invenergy. A PPA is a contract between the buyer and seller of energy for a specific amount of energy at a specific price. By guaranteeing the purchase of 225 Megawatt-hour (MWh), Equinix enabled these providers to complete the build out of their wind farm projects in Oklahoma and Texas.[8] Because the energy from the wind power purchase agreement is generated in the middle of the country where the wind is, not where the data centers use it, a mechanism is needed to ‘transfer’ the renewable energy. This is where Renewable Energy Certificates (RECs – see below) come into play.

Renewable Energy Certificates – Once energy enters into the grid, from any source, it is just energy and we lose track of its origin. A Renewable Energy Certificate or REC is issued for every Megawatt-hour (MWh) of electricity generated and delivered to the grid by a renewable energy source. One MWh is enough to power nearly 1,000 homes for a year. RECs are the currency of the renewable energy market – they allow purchasers to demonstrate demand for renewable energy and provide revenue for it. EPA RECs are uniquely numbered, tracked, and retired: one REC cannot be used by another entity. Anyone can buy RECs – individuals and companies that do so are effectively buying green energy on the grid.

With the virtual PPA in place, Equinix is allocated RECs for all the energy it purchases from NextEra and Invenergy. The company applies these credits towards its overall energy use at its data centers across the US. In this way, Equinix is able to buy 100 percent renewable energy, even if it isn’t locally available at all their sites. The RECs allow Equinix to signal to the market they are a buyer of green energy. And by financing additional wind power to come online via the PPA, Equinix is contributing to the demand for renewable energy and changing the way the cloud is powered.

Multi-Stakeholder Collaboration

Collaboration is critical to greening the grid. Companies like Equinix, Digital Realty and Iron Mountain have played a crucial role as data center leaders in the pursuit of renewable energy. Equinix wanted to help their technology tenants by joining the RE100, an alliance of companies committing to using 100 percent renewables that includes the big tech firms, Google, Apple, and Microsoft. Digital Realty and Iron Mountain collaborated with Facebook and Amazon as part of the Renewable Energy Buyers Alliance (REBA). REBA is organized by four non-profits, including Rocky Mountain Institute, World Resources Institute, World Wildlife Fund and Business for Social Responsibility (BSR). REBA coordinates customers, suppliers, and policymakers to identify barriers to buying clean and renewable energy and develop solutions to meet growing demand.

It is great to see public companies collaborate with their competitors, with their customers, and with non-profits to drive adoption of more renewables. Companies rely on RECs and PPAs because a city, a county, or a state’s local energy mix is still not green enough. These financial instruments are structured for innovation to circumvent whatever obstacles legacy utility companies have in place. Ultimately, for the grid to get greener, utilities will have to change and for that, new regulation and policy is needed. Investors have a critical voice here. By supporting companies that are committed to renewables, pressuring those that aren’t, and asking more from utilities and regulators, investors can amplify the multi-stakeholder approach to transition to a low carbon economy.

Article by Sam Adams, CEO and co-founder of Vert Asset Management. He also chairs the Investment Research Group. Sam leads the development of new products to help make sustainable investing easier for investors. He has been a featured speaker on sustainable investing at financial advisor conferences in the US, UK, Europe, and Australia. Prior to launching Vert, Sam spent almost 20 years working at Dimensional Fund Advisors. He started Dimensional’s European Financial Advisor Services business and led it for 10 years. Sam was part of the team that created Dimensional’s first ESG strategies, the Sustainability Core funds that are offered in the US. He also led the development and launch of Dimensional’s Global Sustainability Core Fund in Europe.

Sam has a BA in Philosophy from the University of Colorado, Boulder and an MBA in Finance from the University of California, Davis. Sam is an avid mountaineer and cyclist, and is very passionate about the environment. He lives in Mill Valley, CA with his wife and three children.

[2] Greenpeace (2017). “Clicking Clean: Who is Winning the Race to Build a Green Internet?” Greenpeace, p.5. Accessed at: http://www.clickclean.org/usa/en/

The Vert Global Sustainable Real Estate Fund only holds publicly traded REITs. The Fund does not hold other types of public companies including Google, Apple, Microsoft, Salesforce. The Fund does not invest in non-profit organizations including Greenpeace, Rocky Mountain Institute, World Resources Institute, World Wildlife Fund and Business for Social Responsibility. The Fund does not invest in energy companies including NextEra or Invenergy. Fund holdings and sectors are subject to change at any time and should not be considered a recommendation to buy or sell any security.

Mutual fund investments involve risk. Principal loss is possible. Investors should be aware of the risks involved with investing in a fund concentrating in REITs and real estate securities, such as declines in the value of real estate and increased susceptibility to adverse economic or regulatory developments. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. A REIT’s share price may decline because of adverse developments affecting the real estate industry. REITs may be subject to special tax rules and may not qualify for favorable federal tax treatment which could have adverse tax consequences. The Fund’s focus on sustainability may limit the number of investment opportunities available to the fund and at time the fund may underperform funds that are not subject to similar investment considerations.

The Vert Global Sustainable Real Estate Fund’s investment objectives, risks, charges, and expenses must be considered carefully before investing. The statutory and summary prospectuses contain this and other important information about the investment company, and may be obtained by calling 1-844-740-VERT or visiting www.vertfunds.com . Read carefully before investing.

The Vert Global Sustainable Real Estate Fund is distributed by Quasar Distributors, LLC.

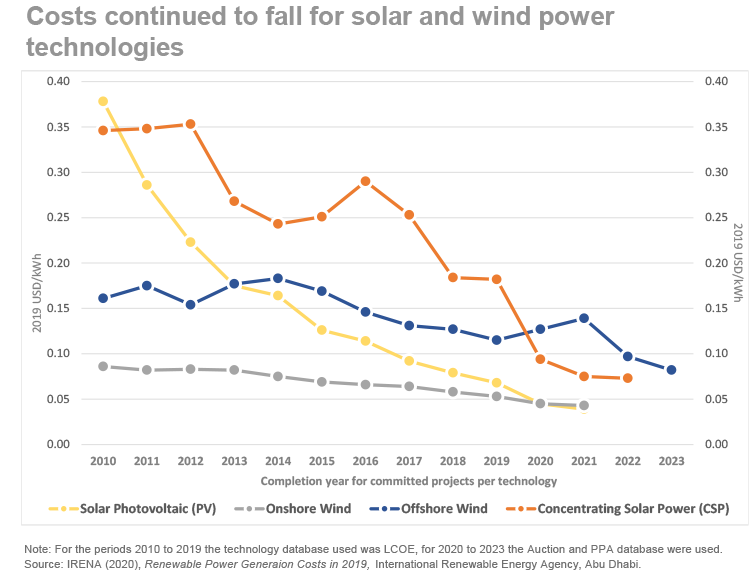

The last decade was quite a remarkable period for renewable energy growth. In 2019, estimates indicate new capacity additions were slightly more than 70 percent renewables and over half of newly commissioned utility-scale renewable power generation provided electricity at a lower cost than the cheapest new fossil fuel powered source.[1]These are significant milestones, especially so, given that they are driven by the incredible cost declines that occurred during the decade. The chart below illustrates these cost declines and Solar Photovoltaic (PV) electricity generation stands out with the most dramatic decline, approximately 80 percent. Expectations over the next few years are for further price declines across renewables.

Let us step back and review the efforts and circumstances that brought us to this point. In retrospect it may look obvious and predictable. Yet in 2010, the global economy was still recovering from the financial crisis. Also, a significant amount of venture capital investment in renewable technologies in the U.S. were made in 2006-07, only to be written off over a multiyear period post crisis. It turned out that renewable energy technology was more energy than technology and lofty valuations, high costs, and much needed subsidies were significant hurdles to new investments, certainly in the U.S. Prior to the crisis, many European countries made great strides in deploying renewables, supported by various programs and subsidies.

Fast forward to the middle of the last decade, and cost declines in solar PV were taking hold. Investors could see the potential competitiveness of this renewable source. The laws of supply and demand would drive the growth providing a transition to a low-carbon economy. Battery storage prices, vital to deploying renewables, also experienced price declines. These factors gained traction and greater renewables growth did indeed occur.

What drove these cost declines? The cost curves pictured in the chart above depict the levelized cost of energy (LCOE), often referred to as the levelized cost of electricity. LCOE is the average total cost of project per unit of total electricity generated. The LCOE allows one to compare various energy-producing sources on a “level” playing field. It also illustrates the breakeven point of a project. It works as a net present-value calculation and allows developers to compare lifetime costs. Thus, many assumptions are embedded in these calculations.

Price declines can be driven by a variety of factors including innovation, “learning” (i.e., improvements due to experience), supply chain improvements, equipment cost declines and economies of scale. The degree to which each of these factors impacted renewables pricing has varied across the different renewable sources. For example, utility-scale solar PV module price declines have been the key determinant of declining LCOE. In onshore wind, technological innovation in turbine design has been a significant factor. The “learning” that results in greater capacity utilization depends, in part, upon greater deployment.

The Outlook: Renewables’ competitiveness with fossil fuels is strong, driven by considerable innovation, learning and economies of scale. We believe that the transition to a low-carbon economy is happening and will continue to happen. This happens over decades, with investors increasingly discounting this long-term trend. Corporate leaders have largely embraced this outlook and individual and institutional investors have turned to ESG strategies in part to avoid risk, capture alpha and drive this low-carbon transition. Developing countries are still in great need of energy and renewables can and should play a significant role. Near term, new renewable projects may even be cheaper than the marginal operating costs of some of the least competitive coal-based plants. Retiring these and replacing with solar PV or onshore wind could lower plant operational costs while reducing carbon emissions.

However, energy growth, in whatever form, is severely challenged by COVID-19 and its economic aftershocks and collateral damage. There is simply no getting around this. Challenged economic growth is an energy-demand shock. This makes deploying and converting to renewables more difficult. It is one thing to add renewable capacity to satisfy growing demand and quite another to replace existing infrastructure while demand is flat, declining, or uncertain, when all eyes are on credit worthiness, and when government stimulus is so heavily relied upon.

Competing needs for funds, calls to close the wealth gap or provide basic support for those in need, falling fossil-fuel exports for export-dependent countries – all of these are headwinds to energy demand. While sun and wind may be “free,” harnessing them, deploying in scale, reaping the benefits of experience are not and these costs are upfront. Renewables are indeed competitive with fossil fuels in many places and situations, and renewable capacity additions place fossil fuel assets, the jobs and supply chains related to these fossil fuel assets at greater risk. How will fossil fuel companies act going forward? Will they go the way of coal or embrace new strategies?

Our Strategy: At Dana Investment Advisors, we are focused on identifying and investing in the strongest players in this field. That is, we seek entities that have experienced leadership, an excellent track record in project development, better demographic geographies, strong balance sheets, and demonstrated success in funding R&D and bringing these investments to fruition. Those companies capable of navigating the current demand shock and playing the long game, can succeed. The need for innovating and delivering reliable and affordable clean energy solutions has never been greater, and we expect the gap between the strongest players and all others to grow larger through a more challenged economic backdrop.

Article by Lydia Miller, Senior Vice President and Portfolio Specialist with Dana Investment Advisors (www.danainvestment.com) and focuses on the Firm’s Sustainability and ESG investment strategies. Prior to joining Dana, Lydia was a Managing Director at Big Path Capital (formerly Watershed Capital Group, a certified B Corporation). She was a Managing Director at UBS where she managed a global sustainability equity fund. Lydia is an advisor for Equarius Risk Analytics LLC and guest lectures at various universities on topics related to sustainability and portfolio management. Lydia graduated summa cum laude from the Pennsylvania State University and has an MBA in Finance and International Business from the University of Chicago.

Footnote

[1] Source: IRENA.Org Article: How Falling Costs Make Renewables a Cost-effective Investment Date: June 2, 2020

Amid COVID-19, the Investor Alliance’s latest guidance helps investors get the ‘people part’ of ESG right.

The Investor Alliance for Human Rights has recently published a new Investor Toolkit on Human Rights for asset owners and managers to address risks to people posed by their investments. This comes in the midst of the current international COVID-19 crisis, where systemic economic and social inequalities across societies have been laid bare and exacerbated, and the precarious foundation that financial markets rely upon is evident now more than ever.

In this context, institutional investors of all sizes have a responsibility as well as an opportunity to support recovery and positively contribute to new systems grounded in respect for human rights – what every individual is entitled to in order to live a life of fundamental welfare, dignity, and equality.

While a growing number of mainstream investors are integrating environmental, social, and governance (ESG) criteria into their investment activities, many are not. Even when ESG factors are considered, addressing risks to people as part of these efforts remains widely neglected.

“In this global crisis, we see why investment-as-usual must change. An essential step in this process is recognizing that institutional investors, even minority shareholders, have a responsibility to address the risks to people present in their investment value chains. To do this, investors should know the human rights risks connected to their investment portfolios and show how they are taking action to manage those risks in line with globally agreed upon standards,” said Paloma Muñoz Quick, former Director of the Investor Alliance for Human Rights.

The expectation that investors, like all business actors, respect human rights is outlined by the UN Guiding Principles on Business in Human Rights, unanimously endorsed by governments in the UN Human Rights Council in 2011.

This expectation is also increasingly embedded into legal requirements impacting financial markets across the world. In particular, the European Union (EU) redefined the roles and responsibilities of institutional investors as financial actors by recently adopting a new set of rules requiring European investors to disclose the steps they have taken to address the adverse impact of their investment decisions on people and the planet.

“For European investors, integrating human rights considerations into our investment activities is no longer a ‘nice-to-have’ proposition. The Investor Toolkit provides timely and much-needed practical guidance for helping investors apply the UN Guiding Principles and meet emerging EU requirements calling on investors to disclose due diligence efforts to manage risks to people throughout the investment lifecycle,” said Carola van Lamoen, Head of Active Ownership and Executive Director at Robeco.

The integration of the UN Guiding Principles into other leading responsible business standards such as the OECD Guidelines for Multinational Enterprises has helped raise awareness and understanding of responsible human rights risk management, providing an approach to pragmatic and meaningful governance processes that support all ESG-related activities.

“Today more than ever we are seeing that resiliency and sustainability in business practices and economic models are crucial to responding to and mitigating global challenges. Investors can play an important role in driving responsible business practices that create long term value and avoid causing harm to society and the environment. To support investors in this endeavor, in 2017 the OECD introduced due diligence guidance on Responsible Business Conduct for Institutional Investors, which has been formally endorsed by 49 governments and created in close consultation with leading investment practitioners and experts. We welcome the Investor Alliance for Human Rights’ Investor Toolkit on Human Rights as another tool for investors to enhance their investment practices and drive positive social and environmental impacts,” said Barbara Bijelic, Legal Expert and Project Lead, Responsible Business Conduct in the Financial Sector at the Organisation for Economic Co-operation and Development (OECD).

While business models and corporate cultures have in many ways contributed to the vulnerability of societies in responding to unprecedented situations such as the current pandemic, responsible companies are experiencing the positive effects of putting people first. In fact, an increasingly wide range of research shows the correlation between corporate attention to human rights risks and corporate financial performance.

“Addressing human rights risks is an important component of financially responsible and sustainable investment strategies. By assessing human rights risks during investment-decision making and engaging portfolio companies to promote the adoption of human rights policies and due diligence, we are better able to avoid the financial and reputational risks associated with unmanaged human rights harms in investment portfolios,” said Lauren Compere, Managing Director and Director of Shareowner Engagement at Boston Common Asset Management.

The Investor Alliance for Human Rights is a collective action platform for responsible investment that is grounded in respect for people’s fundamental rights. Its members represent over US$4 trillion in assets under management and 18 countries. Members include asset management firms, public pension funds, trade union funds, faith-based institutions, family funds, and endowments. The Investor Alliance is an initiative of the Interfaith Center on Corporate Responsibility (ICCR).

In light of COVID-19, the need for corporations to take a collaborative approach to solve the world’s greatest challenges has never been more apparent. This is especially true for technology companies as data and information play a crucial role in helping to track, diagnose and treat this pandemic, and will continue to do so as we look to get ahead of future global challenges.

Intel has a long history of integrating corporate responsibility efforts into our operations, and it’s hard to believe that nearly 10 years have passed since we developed our 2020 corporate responsibility goals. I am pleased to share that we achieved nearly all of them. Our latest Corporate Responsibility Report details our efforts, but there are a few accomplishments I’d like to highlight:

• Addressing climate change and sustainable water use are priorities for Intel given the energy and water intensity of semiconductor manufacturing. The United Nations reports that climate change is affecting every country on Earth — disrupting economies and changing weather patterns; and greenhouse gas emissions are at their highest levels. The UN also reports it is impacting our water, resulting in unpredictable supply, impaired quality and depleted sources. Some of the ways we have addressed climate change are by increasing our use of green power to 71% globally and reducing our direct carbon emissions by 39% on an intensity basis from a 2010 baseline. Since 2000, we have reduced our Scope 1 and 2 emissions 31% on an absolute basis[1], even as we significantly expanded our manufacturing capacity. We also exceeded our goal to reduce our water use below 2010 levels on an intensity basis[2], achieving a 38% decrease. In partnership with environmental nonprofit organizations, we restored one billion gallons of water to local watersheds.

• Advancing inclusion is core to our culture and essential to innovation. A recent Gartner survey found that 85% of diversity and inclusion leaders cited organizational inclusion as the most important talent outcome of their efforts, yet only 57% of organizations are currently using that metric to track progress. We set ambitious 2020 goals and committed $300 million to accelerate progress at Intel and across the technology industry. We reached full representation[3] in our U.S. workforce for women and underrepresented minorities two years ahead of schedule as well as global gender pay equity. We also met our goal to increase annual spending with diverse suppliers to $1 billion and reached 5 million women through our technology empowerment programs.

I am proud of what we accomplished, but the world has changed significantly since we set the original goals. We need integrated corporate responsibility strategies in which companies use collaborative models to drive increased value creation and societal impact. The current pandemic has brought these new approaches into sharper focus as the challenges we face are simply too complex to be solved by any single organization.

With this in mind, we launched an integrated approach to create our 2030 goals and strategy. In order to drive a companywide mindset for corporate responsibility, we are leveraging the expertise and skills of many employees across multiple departments and regions. We also integrated input from external stakeholders, including our customers, investors, suppliers and community members, to ensure partnership and collaboration are at the heart of our work.

The result is Intel’s new RISE strategy and 2030 goals. Through this strategy, we strive to create a more responsible, inclusive and sustainable future, enabled through our technology and the expertise and passion of our employees. We will extend our impact by partnering with others in the technology industry and beyond, including government, NGOs and policymakers, to tackle key global challenges. Our RISE strategy is:

• Lead in advancing safety, wellness and responsible business practices across our global manufacturing operations, our value chain and beyond. One of our new goals in this area will scale our supply chain responsibility programs to 100% of our Tier 1 contracted suppliers and higher-risk Tier 2 suppliers, helping us to positively impact the lives of more people in the global supply chain. We will also work across our industry to leverage our best-known methods from our work on conflict minerals to extend responsible minerals sourcing across a wider range of materials to advance respect for human rights.

• Inclusive. Advance diversity and inclusion across our global workforce and industry, and expand opportunities for others through technology inclusion and digital readiness initiatives. As we look to 2030, we will increase women in technical roles to 40% and double the number of women and underrepresented minorities in senior leadership. We will also collaborate with our industry to create and implement a Global Inclusion Index. The Index will provide common definitions and data to clearly identify root causes and actions needed to collectively advance progress and build the future pipeline of talent.

• Sustainable. Be a global leader in sustainability and enable our customers and others to reduce their environmental impact through our actions and technology. With our new goals, we challenge ourselves to achieve net positive water use, 100% renewable power, zero total waste to landfills and additional absolute carbon emissions reductions, even as we grow. We will also launch collaborative initiatives to drive additional carbon emissions reductions and sustainable chemistry practices across our industry.

Today, May 14, 2020 marks the beginning of a new era for corporate responsibility at Intel. We stand ready to work with others on our key global challenges to revolutionize how technology will improve health and safety, make technology fully inclusive and expand digital readiness, and achieve carbon neutral computing. We’ll drive to even higher levels of integration and collaboration to build more value for our stakeholders and deliver on our purpose to create world-changing technology that enriches the lives of every person on Earth.

I invite you to learn more about our accomplishments and goals, and how you can join us at www.intel.com/responsibility

Article by Suzanne Fallender, director of Corporate Responsibility, Intel Corporation. In this role, she collaborates with key stakeholders across the company to integrate corporate responsibility concepts into company strategies, policies, public reporting, and stakeholder engagement activities to advance Intel’s corporate responsibility leadership and create positive social impact and business value. Suzanne leads a team of experienced professionals who engage with internal and external groups to review Intel’s corporate responsibility performance and to identify new opportunities to apply Intel’s technology and expertise to address social and environmental challenges. The team also works closely with Intel’s investor relations and corporate governance groups to drive an integrated outreach strategy with investors on governance and corporate responsibility issues. Suzanne has more than 20 years of experience in the field of corporate responsibility and socially responsible investment. During her time at Intel, Suzanne has held a number of corporate responsibility-related roles, including leading programs empowering girls and women through technology. Prior to Intel, Suzanne served as Vice President at Institutional Shareholder Services where she managed the firm’s socially responsible investing division. Suzanne holds an M.B.A. from the W.P. Carey School of Business at Arizona State University and a B.A. from Trinity College in Hartford, CT. She has served on a number of leading industry advisory boards and committees on sustainability and corporate responsibility over the past decade and currently is a member of the Net Impact Board of Directors. Follow Suzanne on Twitter at @sfallender

Footnotes

[1] Absolute basis refers to the total amount of emissions being emitted.

[2] Intensity basis refers to a normalized metric that compares the total emissions target relative to its economic output.

[3] Full representation means that Intel’s workforce now reflects the percentage of women and URMs available in the U.S. skilled labor market.

A new book by William J. Ginn, business strategy consultant and founder of NatureVest at The Nature Conservancy.

To address the climate and biodiversity crises, we must invest trillions in renewing large-scale infrastructure, from energy production to water delivery systems. Only the private sector has the ability to meet that extraordinary level of funding. While the business world has often exploited nature, NatureVest founder William J. Ginn argues that its entrepreneurial talent and financial capital are critical resources for developing solutions to global issues while protecting natural systems.

In Valuing Nature: A Handbook for Impact Investing, Ginn examines the scope of nature-based investing opportunities while presenting a practical overview of their limitations and challenges. With this strategy, the private sector can invest in the sustainable, equitable management of natural capital while earning financial returns.

Ginn presents a new set of nature-based investment areas to help conservationists and investors work together, including green infrastructure, forests, soils, and fisheries. He shows how investing in agriculture can improve the sustainability of our food and how we can use new land conservation tools, such as private investment partnerships, to meet large-scale conservation goals.

He acknowledges critiques of putting financial value on natural assets’ ecosystem services. However, Ginn argues that doing so is crucial to incenting new investments. With natural systems playing a critical role in mitigating climate change, the lack of proper recognition of these systems’ value leads to overuse and underinvestment – the opposite of the work we must due to preserve and restore them.

In the second half of the book, Ginn presents tools for investors and organizations to consider as they develop their own projects and provides tips on how nonprofits can successfully engage with nature-based impact investing. He covers lessons that impact investors can learn from other sectors, such as microfinance, about how to build the case for investing in natural capital. Ginn also offers guidance about raising capital for investment projects, covering key topics including business plans that generate returns, the right corporate structure, and the types of capital needed. Ginn argues that to continue attracting investors, organizations must measure the outcomes of impact investments. Acknowledging the difficulty of measuring results, he analyses the strengths and weaknesses of various metrics. Ginn covers five important legal issues for nonprofits and foundations that sponsor or offer impact investments, including adhering to your organization’s charitable purposes and managing investments from foundations and endowments.

Throughout Valuing Nature, Ginn highlights successful examples of nature-based impact investing in action. Case studies include the water-trading system in Australia’s Murray-Darling River Basin and the stormwater credit market in Washington, DC.

Valuing Nature provides a roadmap for those seeking to improve the management of natural systems through market-based strategies. With the environment degrading, Ginn shows how we can utilize private capital to achieve more sustainable uses of our resources.

William J. Ginn, is a business strategy consultant who has served in senior leadership positions in both nonprofit organizations and businesses. During his tenure at The Nature Conservancy, Ginn served as Chief Conservation Officer and then Executive Vice President, founding NatureVest, a partnership with private investors that has brought over $200 million of investment into conservation projects worldwide. He is the author of the 2005 Island Press book Investing in Nature: Case Studies of Land Conservation in Collaboration with Business.

Just as I was about to head from the kitchen to the office to write an article about Slow Money for this issue of the GreenMoney Journal, a story appeared on CNN about Whoa Nellie Farm in Acme, Pennsylvania. I had no choice but to start here.

When, due to Covid-19 supply chain disruptions, the farm’s Pittsburgh-based milk processor stopped purchasing their milk, they ramped up a 30-gallon-per-hour bottling and pasteurization operation on the farm and put out a call to their community. Before long, there was a line of cars down the street and they were expanding to 45 gallons per hour. “It has been wonderful to see the community coming together like this. Everyone is so happy to get their milk from a local dairy again, to know where their food comes from. No one wants to see us dumping milk…”

Whoa Nellie, indeed. Whoa, pandemic! Whoa, Wall Street! Whoa, Main Street! Whoa empty streets and empty skies! Whoa food grown for export! Whoa fast food and fast money and 30,000 Dow and runaway financialization and globalization! Have we lost our senses?? Will we rush back to business as usual when the pandemic is over? Or will this time be different?

The structural problems of the food system mirror structural problems in finance. Ultra-fast trading and ultra-pasteurization are twins. Over dependence on distant markets and complex intermediation make us insecure.

Thoreau wrote, “A man is wealthy to the extent he can afford to leave things alone.” Leaving aside the rich discussion we could have about that observation, let’s adapt the spirit of it thus: “A community is rich to the extent it can afford to feed itself.”

Whoa Nellie, indeed.

Since 2010, the Slow Money movement has been Whoa Nellie-ing its way towards a systemic response, encouraging groups of individual investors to come together to put money to work in support of small, diversified organic/regenerative farms. I use the backslash there because I am not particularly enamored of the recent rush to the term regenerative. That said, neither am I against it. It’s a perfectly good word. But I am concerned about the way we constantly feel the need to trade in common sense and direct action for new terminology and the latest distant shiny object, whether that object be a financial derivative or a new, fancy name for longstanding principles of sound cultivation and stewardship.

As just one case in point, check out the caption to the photo on the front page of the New York Times, April 22, 1970, the first Earth Day:

I hope formatting will allow you to make it out, but in that photo caption are the words “a call for the regeneration of a polluted environment.”

Folks are now talking about regenerative economics as well as regenerative agriculture. The conversations are elegant, systemic, nuanced. Some come with elaborate models. Some come with formal certification schemes. To which we might wonder, in the spirit of Whoa Nellie, whether we are going to chase the rabbit all the way down the hole until we arrive at Certified Local. Or Certified Common Sense. Or Certified Neighborly. Or Certified Community.

That is coming off a bit crankier than I intend. But I am very concerned about whether we have the wherewithal, here in the home of fast food, here in the home of Wall Street and Silicon Valley, to bend the arc of history, 50 years after the first Earth Day, to take back control of runaway economic forces, runaway forces of globalization and urbanization and industrialization and militarization and commodification and consolidation and intermediation.

Whoa, Nellie!

Slow Money’s contribution to this cultural conversation is local and direct. Since 2010, more than $75 million has flowed, via volunteer-led slow money activities in dozens of communities, to over 750 local, organic farms and food enterprises, in amounts ranging from a few thousand dollars to a few million. Most recently, we’ve seen the emergence of SOIL groups—SOIL as in Slow Opportunities for Investing Locally—that take in charitable donations and make 0% loans by majority vote of donor members.

Eric and Jill Skokan, owners of Black Cat Farm and Black Cat Farm Table Bistro in Boulder, CO received the first 0% loan made by SOIL.

Today, kicked in the gut by the pandemic, we all find ourselves wondering if this time will be different. Earth Day felt different to the 20 million Americans who marched in 1970 in thousands of places around the country. Think about that for a second. 20 million Americans in thousands of places. And it felt different when Greta Thunberg stood in front of the UN General Assembly last fall and admonished us to stop chasing “fairy tales of endless economic growth.” It really did feel different.

For regenerative agriculture to be an effective agent for making things different this time, it will need to be accompanied by a process of re-localizing portions of the food system. For regenerative economics to make things different this time, we are going to have to re-localize meaningful aspects of the economy. When we hear the word regeneration let us also think of the word re-localization. Not as an alternative, but as a complement, empowering acts of completion and rebalancing that have the potential to make things different this time.

As David Brooks observes: “We’ve tried liberalism and conservatism and now we’re trying populism. Maybe the next era of public life will be defined by a resurgence of localism.”

I think of local investing, in general, and slow money, in particular, as vital grounding, a “homecoming” (to borrow from Wendell Berry and Wes Jackson) for the process that began as socially responsible investing and then became double-bottom-line investing and then triple-bottom-line investing and then impact investing. We are marching towards the greatest AHA! moment of all time. An awakening, an inspiration strong enough to break us out of the shell of Making a Killing so that we can breathe the air of Making a Living, connecting us in new ways to one another, to the places where we live, to the land. . .all the way down to the life in the soil, teeming with life. Hence my forthcoming book…

AHA!: Fake Trillions, Real Billions, Beetcoin

and the Great American Do Over:

If the need to relocalize the food supply was not widely apparent prior to the pandemic, it is now, as supply chain disruptions result in millions of gallons of milk being dumped daily and traffic jams at food banks around the country. In response to these disruptions, we can double down on the speed, power and scale of factory food production. We can call in the national guard. We can import a little less apple juice from China.[1] But going beyond such fixes, we also need to address the underlying vulnerabilities of a system that was designed not to feed the local populace, but to produce prodigious quantities of cheap agricultural commodities for export.

The next 50 years will be the epoch when diversity, decentralization, deceleration, and disintermediation come to the fore, not as replacements for the industrial-strength efficiencies of globalization, but as vital components of rebalancing, relocalization and resilience.

As we consider all of this, let’s use the current moment to realize that we were shutting down long before the Shut Down.

We were shutting down small towns. We were shutting down small farms. We were shutting down local newspapers. We were shutting down diversity in the name of efficiency. We were shutting down culture in the name of commerce. We were shutting down trust. We were shutting down home and hearth in favor of fast food. We were shutting down Here in favor of Everywhere and Nowhere. We were shutting down the real in favor of the fake.

Now may or may not be the moment to open up this part or that part of the economy. But it is definitely the moment to do what we can to begin making sure this time is different. Which means opening our hearts and minds to whole new ways of investing, in things that we understand, near where we live, starting with food.

Woody Tasch is the author of Inquiries into the Nature of Slow Money: Investing as if Food, Farms, and Fertility Mattered (Chelsea Green) and SOIL: Notes Towards the Theory and Practice of Nurture Capital (Slow Money Institute). Tasch is former chairman of Investors’ Circle, a nonprofit angel network that has facilitated more than $200 million of investments in over 300 early-stage, sustainability-promoting companies. As treasurer of the Jessie Smith Noyes Foundation in the 1990s, he was a pioneer of mission-related investing. He was founding chairman of the Community Development Venture Capital Alliance. Utne Reader named him “One of 25 Visionaries Who Are Changing Your World.”

FOOTNOTES

Some 60% of apple juice consumed in the U.S. is imported from China. From 1970-2005, total U.S. imports of apple juice increased from 27 million gallons to 428 million gallons. From 1995-2005, U.S. imports of apple juice from China increased from 2 million gallons to 253 million gallons. (Fonsah and Muhammad, Journal of Food Distribution Research, March, 2008)

Located on the “quiet side” of Maine’s Mount Desert Island, Tremont is a fishing town with a significant influx of summer tourism in typical years, thanks to nearby Acadia National Park. While the town is small, with only 1,529 year-round residents, its leadership values using natural resources sustainably. So, when the town was looking for ways to reduce the fiscal and environmental costs of its energy needs, it made sense to look to solar.

Located on the “quiet side” of Maine’s Mount Desert Island, Tremont is a fishing town with a significant influx of summer tourism in typical years, thanks to nearby Acadia National Park. While the town is small, with only 1,529 year-round residents, its leadership values using natural resources sustainably. So, when the town was looking for ways to reduce the fiscal and environmental costs of its energy needs, it made sense to look to solar.

Buildings consume 40 percent of global energy and create 30 percent of global energy-related greenhouse gas emissions; they are a big part of the climate change puzzle.

Buildings consume 40 percent of global energy and create 30 percent of global energy-related greenhouse gas emissions; they are a big part of the climate change puzzle.

Just as I was about to head from the kitchen to the office to write an article about Slow Money for this issue of the GreenMoney Journal, a story appeared on CNN about Whoa Nellie Farm in Acme, Pennsylvania. I had no choice but to start here.

Just as I was about to head from the kitchen to the office to write an article about Slow Money for this issue of the GreenMoney Journal, a story appeared on CNN about Whoa Nellie Farm in Acme, Pennsylvania. I had no choice but to start here.