A Rare Corner of Finance Where Women Dominate

Once a year, a small group of executives who control trillions of dollars in American companies meet for lunch in Manhattan. Among the things they discuss: pushing for greater say in how companies are run.

It is an elite gathering, but you will not see a single man in a suit in the room. The event, called the Women in Governance lunch, underscores a rare corner in finance where women dominate.

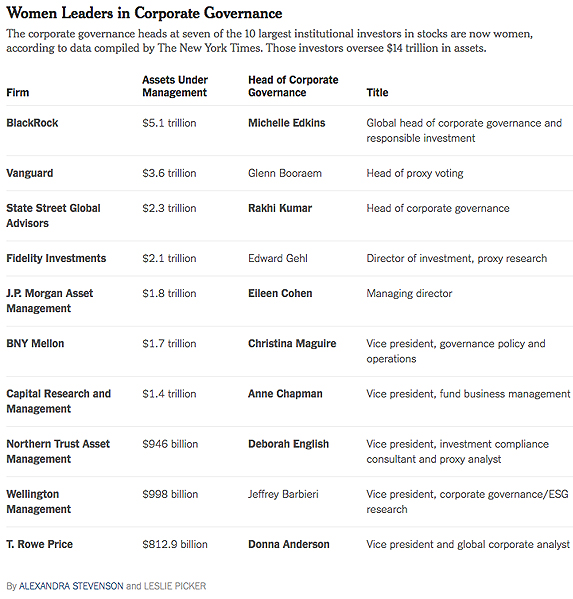

Women hold the top positions in corporate governance at many of the biggest mutual funds and pension funds — deciding which way to vote on the directors of a company board. They make decisions on behalf of teachers, government workers, doctors and most people in the United States who have a 401(k). The corporate governance heads at seven of the 10 largest institutional investors in stocks are now women, according to data compiled by The New York Times. Those investors oversee $14 trillion in assets.

Corporate governance is playing a growing role within the broader ecosystem of corporate America. Each spring, publicly traded companies hold shareholder meetings and outline business strategy for the coming year. Shareholders like BlackRock, T. Rowe Price and State Street vote on corporate strategy and issues including company board appointments and compensation.

Their votes can go a long way, given the huge stakes these institutions control in United States companies. BlackRock holds a stake greater than 5 percent in 75 of the 100 largest companies, according to data compiled by Jerry Davis, a professor at the University of Michigan Ross School of Business. State Street has more than than 5 percent of 23 of the largest companies, while Capital Group owns more than 5 percent of 20 of the biggest companies.

That power, however, is rarely wielded to confront companies. Most of the time, these huge institutional investors choose to vote with management.

And their approach contrasts sharply with that of brash activist billionaires like William A. Ackman and Daniel S. Loeb, who have made a name for themselves as corporate agitators. These investors bring about change by theatrically pounding on the front doors of companies and using the public court of opinion to bully companies into changing their strategies.

Still, the heads of corporate governance at institutional giants say they are working quietly behind the scenes to advocate for greater shareholder rights.

When Donna F. Anderson and her team at T. Rowe Price became concerned at a growing list of public companies that were creating more than one class of stock, effectively giving corporate insiders greater influence and say in the company, they used their vote to make a point. Ms. Anderson, who is the head of corporate governance, created a policy to vote against key directors at companies with dual-class share structures like that at Facebook.

Now, Ms. Anderson’s team is weighing whether to create a similar policy for gender diversity on corporate boards.

“We have an interest in seeing more women on boards because there is data that a more diverse board makes better decisions,” said Ms. Anderson, who was at Invesco before T. Rowe Price and has been working in the field of corporate governance for two decades.

Efforts by mutual funds to change the behavior of a company by using the power of a proxy vote is a fairly recent phenomenon. For decades, powerful institutional investors automatically rubber-stamped the decisions of corporate management and boards. At the same, many top executives paid little attention to the concerns of their shareholders.

“Many years ago, for every 10 letters we wrote, we generally heard back from half,” Ms. Anderson said. “Now it’s 100 percent.” Today, companies in which T. Rowe Price holds a large stake will even reach out to the firm unprompted.

The 2008 financial crisis was a turning point for shareholders, said Anne Sheehan, the director of corporate governance at California State Teachers’ Retirement System, the public pension fund.

Ms. Sheehan joined the pension fund, Calstrs, in October 2008, in the depths of the financial crisis after the collapse of Lehman Brothers. “Talk about hitting the ground running and seeing what the impact of that crisis was doing to our portfolio,” she said.

The experience was an eye-opener. “I saw it as an opportunity to make our voices known in the debate,” Ms. Sheehan said. “What were these directors doing on our behalf? How could shareholders speak up?”

The crisis, she added, “really brought home the prevalence of the ‘Old Boys Network’ inside the board rooms of these financial firms which resulted in too much group think.”

The corporate governance team at Calstrs regularly questions companies on a range of issues including gender diversity and the pay gap between the top executives at a company and the most junior employees. Having women in positions of governance has helped bring these issues to the forefront of the discussion at companies, Ms. Sheehan said.

“It reminded me of the old adage: If you want to get something done, put a woman in charge,” she added.

At BlackRock, Michelle Edkins and her team of 30 analyze whether certain corporate directors are being paid too much and whether they have overstayed their terms. If there is a problem, they begin by opening a dialogue with the company.

Ms. Edkins, who trained as an economist in New Zealand and took her first position in corporate governance in 1997 by answering an ad in The Financial Times, said women tended to be less confrontational than men, making it easier to address a problem and try to fix it in this way.

“We don’t meet with C.E.O.s and tell them how to remedy the problem,” she said. “It’s a stylistic difference and my observation is that this constructive challenge comes more naturally to women.”

But to some critics, this approach is not yielding change fast enough.

BlackRock’s track record on voting against corporate management reveals that it is taking a slower approach to pushing for change. For example, on the issue of executive pay, during the most recent reporting period ending on June 30, BlackRock voted 96.3 percent of the time to support compensation policies across the Standard & Poor’s 500-stock index, according to Proxy Insight.

It also voted against every shareholder proposal relating to diversity, environment, governance and social concerns over the last year, according to Proxy Insight.

The record is not much better at other top institutional investors.

Nick Dawson, a co-founder of Proxy Insight, said that while investors treat issues related to environmental, social and governance policies, known in industry parlance as E.S.G., very seriously, “there is a clear preference for behind-the-scenes engagement on these issues.” “Asset managers prefer to ensure that management teams are capable of dealing with E.S.G. issues in-house, rather than by applying external pressure,” he said.

Still, BlackRock said that it voted against pay practices or compensation committee members at 10 of the 50 companies where executives were paid the most during the most recent reporting period.

In one recent case involving Mylan, the company that makes the allergy treatment EpiPen, BlackRock spent two years engaging with the board over the generous pay packages of top executives. When this did not yield a change to compensation, Ms. Edkins’ team voted against the three top-earning directors.

And other investors like the activist hedge fund Elliott Management said that it had become much easier to engage with companies.

“When an activist shows up to a situation, having these engaged, thoughtful leaders involved in the discussion helps the company and the activist get to a collaborative solution,” said Jesse Cohn, the head of United States equity activism at Elliott. This, he added, happens “well in advance of a proxy contest.”

There is concern that on the subject of gender, women are less likely to push for greater diversity. Some women in high-power corporate governance positions said that they preferred not to bring up gender as an issue in discussions with management on concern they will be perceived to have an agenda.

But some experts say there is tremendous potential for the network of women in corporate governance to make a bigger difference.

“If there is an old girls’ network so to speak with so much authority in corporate governance, this is an opportunity to create an agenda for greater diversity through a formalized means,” said Mr. Davis, at the University of Michigan.

While women like Ms. Edkins are fighting behind the scenes to bring more women onto the boards of America’s biggest companies, they are struggling with an entirely different diversity challenge of their own: the lack of men in the field of corporate governance.

“It’s counterintuitive in finance,” Ms. Edkins said. “But when we are hiring, we need to really push that diversity to make sure we have men on the slate.”

Read the full article with numerous links and photos at: www.nytimes.com/2017/01/16/business/dealbook/women-corporate-governance-shareholders.html