Facing Our Relationship with Money Can Change Us

![]() I have been working with people and their finances for almost twenty years now, and one thing I know for certain: Each person’s relationship with money is unique and powerful, whether they choose to recognize it or not. I have also noticed that those who are willing to accept and work with the realities of their relationship with money generally lead happier and more balanced lives.

I have been working with people and their finances for almost twenty years now, and one thing I know for certain: Each person’s relationship with money is unique and powerful, whether they choose to recognize it or not. I have also noticed that those who are willing to accept and work with the realities of their relationship with money generally lead happier and more balanced lives.

My experience is no exception, and it was indeed my own (at first reluctant) willingness to look at my somewhat twisted relationship with money and its connection to the rest of my life that lead me on the path to helping others “integrate money and meaning.”

Angst around money was a pervasive part of my childhood and young adulthood, not because I didn’t have much, but because I did. I grew up in a one-stoplight town in rural Pennsylvania, where most people made their living by farming or manufacturing. But I was different because it was MY family’s manufacturing business that employed a lot of the residents. We lived in a large house, drove nice cars, were expected to go to a prestigious college, and took really nice vacations. Growing up, I learned quickly that this was not the norm for others in the area, and the differences could be stark.

I also learned that while money certainly bought options, it did not deliver happiness. I am grateful for the support I received from my family and recognize that it helped me get where I am today, but it was not a happy childhood. My family provided me with many resources and an element of love, but it also included dysfunction, regrets, secrets, and betrayal. Our affluence not only didn’t prevent such dysfunction, it exacerbated it.

When it came time for me to go to college, I chose to go to a state school (in defiance of expectations), but I was still dependent on my family’s money, which caused me a lot of conflict. Plus I knew almost nothing about managing money. I began to feel a terrible tension between having too much money and not having enough, at the same time recognizing that none of the money was really mine to begin with. I started to become politically active and eventually majored in political philosophy. Once again, I was surrounded by people barely making it while that was clearly not the case for me, and it made me uncomfortable.

It took me many years to pull away from the tendrils of my family’s money. At first, I did work in the family business, but after several years I severed ties. It was at this point that my life took an unusual turn. I grew up Roman Catholic, but left the faith when I went to college. But when I was 28 years old and feeling exceptionally untethered, it suddenly hit me that I would make a really good pastor or priest. This bolt of insight struck me as truly ludicrous, considering the fact that I am a woman and a lesbian. But I paid attention to that “call” and went on to get an MDiv from Emory University and finish all but my dissertation for a PhD in religious studies.

This was a time of great growth and positive change for me, though I didn’t end up being a pastor or even a professor as I once thought I would. In looking back, I see now that one sticking point for me was money. I wasn’t consciously thinking about it. I was just thinking about who I was supposed to be, how to connect to the divine, and – of course – how to make a living; in other words – how to have money.

At the age of 37, I found myself at a crossroads. I had a family by then, but in some ways my life was in shambles. I had done at least one thing right though; I had added meditation to my daily routine. One day as I sat meditating, I seemed to be wrestling more than usual with my unruly thoughts, most of which were worries about money. Then out of the blue, the waters of my mind calmed and a message emerged: “Get up and deal with your money.” At first, I resisted – this couldn’t be “right” – money and spiritual practice don’t mix. But soon I stopped resisting, and the message became clear: “Get up and deal with your money.”

After the meditation session ended, I lingered over what had just happened. It seemed important, so I decided to listen. I began by looking realistically at my own financial situation and making changes. I also took a good look at my past experiences with money and how they had formed me. Later, I took the trainings necessary to become a financial advisor. Financial planning seemed to be a way to help others seek a deeper level of integration in their lives, and it aligned with my diverse background. I started a wealth management practice and wrote a book to help others understand their financial lives and connect them to their values and spirituality.

After the meditation session ended, I lingered over what had just happened. It seemed important, so I decided to listen. I began by looking realistically at my own financial situation and making changes. I also took a good look at my past experiences with money and how they had formed me. Later, I took the trainings necessary to become a financial advisor. Financial planning seemed to be a way to help others seek a deeper level of integration in their lives, and it aligned with my diverse background. I started a wealth management practice and wrote a book to help others understand their financial lives and connect them to their values and spirituality.

Like many people, I was taught growing up that religion/spirituality went in one pigeonhole and everything else (money for instance) had its own separate space. I no longer believe in those lines. When I started my financial profession, I saw there was much more to it than the usual figures and formulas. The conversations around money I was having with people intertwined with the larger tapestry of their lives, including their spiritual lives, yet there was no opportunity to address this. There was not even a framework on which to envision the connection.

Developing this framework has been the focus of my work and life ever since: helping people (including myself) live inside our society’s complex money system without being utterly consumed by it, instead working toward a level of integrity, peace, balance, and meaning.

Article by Maggie Kulyk, author of Integrating Money and Meaning: Practices for a Heart-Centered Life and CEO and Founder of Chicory Wealth, a private wealth advisory practice offering holistic Financial Life Planning services to individuals and nonprofit organizations across the country.

In most respects, other than the occasional “I’m not made of money”, my mother tried to protect us from the financial struggles that she encountered during those years. We purchased our Christmas tree on Christmas Eve because it was cheaper then. On the day after Christmas, my grandmother would head downtown to the fancy department stores to buy gifts and things for next Christmas. That was the day of the deep discounts. On regular occasions we would pile into a neighbor’s car and head over to Two Guys in New Jersey, where we bought all of our clothing, appliances and anything else we could load in the car, at very discount prices. If it wasn’t at Two Guys or Woolworths, then we didn’t get it. So that meant no brand name underwear, jeans, sneakers. The only concession to that was for my Converse sneakers, which I was allowed to get if I could pay the amount above what the store brand cost.

In most respects, other than the occasional “I’m not made of money”, my mother tried to protect us from the financial struggles that she encountered during those years. We purchased our Christmas tree on Christmas Eve because it was cheaper then. On the day after Christmas, my grandmother would head downtown to the fancy department stores to buy gifts and things for next Christmas. That was the day of the deep discounts. On regular occasions we would pile into a neighbor’s car and head over to Two Guys in New Jersey, where we bought all of our clothing, appliances and anything else we could load in the car, at very discount prices. If it wasn’t at Two Guys or Woolworths, then we didn’t get it. So that meant no brand name underwear, jeans, sneakers. The only concession to that was for my Converse sneakers, which I was allowed to get if I could pay the amount above what the store brand cost.

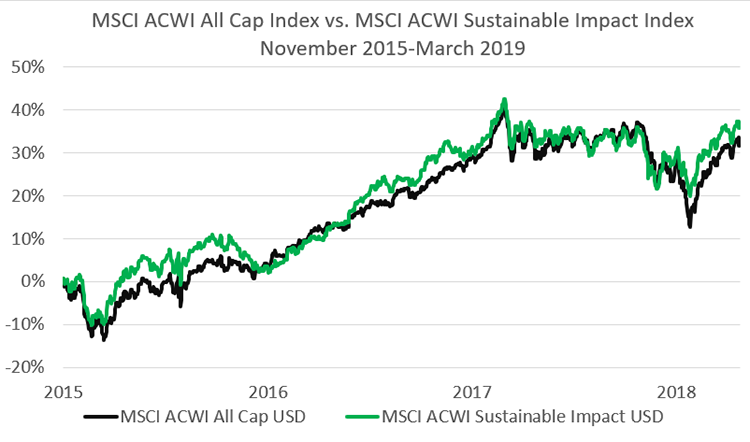

The two urgent environmental problems that will define this millennium and our lifetimes are climate change and biodiversity loss. Although both are the result of the actions of mankind, they are distinct issues and their consequences are, inextricably linked. The detrimental effects of biodiversity loss contribute to the magnitude of the climate change crisis, while climate change exacerbates biodiversity loss. Examining the nexus of these challenges is valuable to academics, scientists, and investors alike with a shared interest in finding solutions that simultaneously mitigate both challenges while ensuring the future sustainability of the planet.

The two urgent environmental problems that will define this millennium and our lifetimes are climate change and biodiversity loss. Although both are the result of the actions of mankind, they are distinct issues and their consequences are, inextricably linked. The detrimental effects of biodiversity loss contribute to the magnitude of the climate change crisis, while climate change exacerbates biodiversity loss. Examining the nexus of these challenges is valuable to academics, scientists, and investors alike with a shared interest in finding solutions that simultaneously mitigate both challenges while ensuring the future sustainability of the planet.